How much money would it take for you to give up internet? …for the rest of your life? … and maybe much more important; How much do you want to pay for internet? The following cool video URL “Would you give up the Internet for 1 Million Dollars” hints towards both of those questions and an interesting paradox!

The perception of value is orders of magnitude higher than the willingness to pay, i.e.,

“I would NOT give up Internet for life for a Million+ US Dollars … oh … BUT… I don’t want to pay more than a couple of bucks for it either” (actually for a mature postpaid-rich market the chances are that over your expected life-time you will pay between 30 to 40 thousand US$ for mobile internet & voice & some messaging).

Price plans are fascinating! … Particular the recent data-centric price plans bundling in legacy services such as voice and SMS.

Needles to say that a consumer today often needs an advanced degree in science to really understand the price plans they are being presented. A high degree of trust is involved in choosing a given plan. The consumer usually takes what has been recommended by the shop expert (who most likely doesn’t have an advanced science degree either). This shop expert furthermore might (or might not) get a commission (i.e., a bonus) selling you a particular plan and thus in such a case hardly is the poster child of objectiveness.

How does the pricing experts come to the prices that they offer to the consumer? Are those plans internally consistent … or maybe not?

It becomes particular interesting to study data-centric price plans that try to re-balance Mobile Voice and SMS.

How is 4G (i.e., in Europe also called LTE) being charged versus “normal” data offerings in the market? Do the mobile consumer pay more for Quality? Or maybe less?

What is the real price of mobile data? … Clearly, it is not the price we pay for a data-centric price plan.

A Data-centric Tale of a Country called United & a Telecom Company called Anything Anywhere!

As an example of mobile data pricing and in particular of data-centric mobile pricing with Voice and SMS included, I looked at a Western European Market (let’s call it United) and a mobile operator called Anything Anywhere. Anything Anywhere (AA) is known for its comprehensive & leading-edge 4G network as well as several innovative product ideas around mobile broadband data.

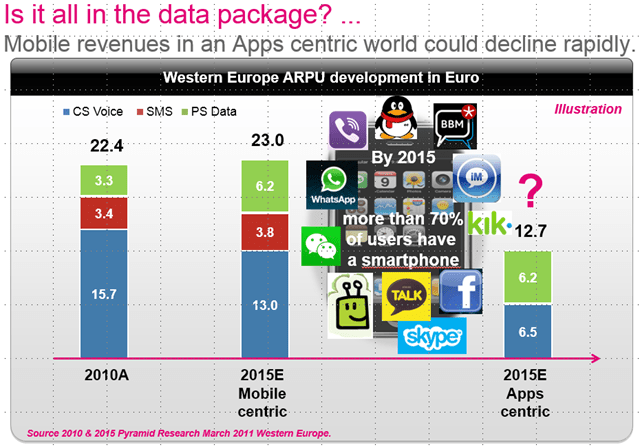

In my chosen Western European country United, voice revenues have rapidly declined over the last 5 years. Between 2009 to 2014 mobile voice revenues lost more than 36% compared to an overall revenue loss of “only” 14%. This corresponds to a compounded annual growth rate of minus 6.3% over the period. For an in depth analysis of the incredible mobile voice revenue losses the mobile industry have incurred in recent years see my blog “The unbearable lightness of mobile voice”.

Did this market experience a massive uptake in prepaid customers? No! Not at all … The prepaid share of the customer base went from ca. 60% in 2009 to ca. 45% in 2014. So in other words the Postpaid base over the period had grown with 15% and in 2014 was around 55%. This should usually have been a cause for great joy and incredible boost in revenues. United is also a market that has largely managed not to capitalize economically on substantial market consolidation.

As it is with many other mobile markets, engaging & embracing the mobile broadband data journey has been followed by a sharp decline in the overall share of voice revenue from ca. 70% in 2009 to ca. 50% in 2014. An ugly trend when the total mobile revenue declines as well.

The Smartphone penetration in United as of Q1 2014 was ca. 71% with 32% iOS-based devices. Compare this to 2009 where the smartphone penetration was ca. 21% with iOS making out around 75+%.

Our Mobile Operator AA has the following price plan structure (note: all information is taken directly from AA’s web site and can be found back if you guess which company it applies to);

- Data-centric price plans with unlimited Voice and SMS.

- Differentiated speed plans, i.e., 4G (average speed advertised to 12 – 15 Mbps) vs. Double Speed 4G (average speed advertised to 24 – 30 Mbps).

- Offer plans that apply Europe Union-wide.

- Option to pay less for handsets upfront but more per month (i.e., particular attractive for expensive handsets such as iPhone or Samsung Galaxy top-range models).

- Default offering is 24 month although a shorter period is possible as well.

- Offer SIM-only data-centric with unlimited voice & SMS.

- Offer Data-only SIM-only plans.

- Further you will get access to extensive “WiFi Underground”. Are allowed tethering and VoIP including Voice-calling over WiFi.

So here is an example of AA’s data-centric pricing for various data allowances. In this illustration I have chosen to add an iPhone 6 Plus (why? well I do love that phone as it largely replaces my iPad outside my home!) with 128GB storage. This choice have no impact on the fixed and variable parts of the respective price plans. For SIM-Only plans in the data below, I have added the (Apple) retail price of the iPhone 6 Plus (light grey bars). This is to make the comparison somewhat more comparable. It should of course be clear that in the SIM-only plans, the consumer is not obliged to buy a new device.

- Figure above: illustrates the total consumer cost or total price paid over the period (in local currency) of different data plans for our leading Western European Mobile Operator AA. The first 9 plans shown above includes a iPhone 6 Plus with 128GB memory. The last 5 are SIM only plans with the last 2 being Data-only SIM-only plans. The abbreviations are the following PPM: Pay per Month (but little upfront for terminal), PUF: Pay UpFront (for terminal) and less per month, SIMO: SIM-Only plan, SIMDO: SIM Data-Only plan, xxGB: The xx amount of Giga Bytes offered in Plan, 2x indicates double 4G speed of “normal” and 1x indicates “normal” speed, 1st UL indicates unlimited voice in plan, 2nd UL indicates unlimited SMS in plan, EU indicates that the plan also applies to countries in EU without extra charges. So PPM20GB2xULULEU defines a Pay per Month plan (i.e., the handset is pay over the contract period and thus leads to higher monthly charges) with 20 GB allowance at Double (4G) Speed with Unlimited Voice and Unlimited SMS valid across EU. In this plan you would pay 100 (in local currency) for a iPhone 6 Plus with 128 GB. Note the local Apple Shop retail price of an iPhone 6 Plus with 128 GB is around 789 in local currency (of which ca. 132 is VAT) for this particular country. Note: for the SIM-only plans (i.e., SIMO & SIMDO) I have added the Apple retail price of a iPhone 6 Plus 128GB. It furthermore should be pointed out that the fixed service fee and the data consumption price does not vary with choice of handset.

If I decide that I really want that iPhone 6 Plus and I do not want to pay the high price (even with discounts) that some price plans offers. AA offers me a 20GB 4G data-plan, pay 100 upfront for the iPhone 6 Plus (with 128 GB memory) and for the next 24 month 63.99 (i.e., as this feels much cheaper than paying 64) per month. After 24 month my total cost of the 20 GB would be 1,636. I could thus save 230 over the 24 month if I wanted to pay 470 (+370 compared to previous plan & – 319 compared to Apple retail price) for the iPhone. In this lower cost plan my monthly cost of the 20 GB would be 38.99 or 25 (40%!) less on a monthly basis.

The Analysis show that a “Pay-less-upfront-and-more-per-month” subscriber would end up after the 24 month having paid at least ca. 761 for the iPhone 6 Plus (with 128GB). We will see later, that the total price paid for the iPhone 6 Plus however is likely to be approximately 792 or slightly above today’s retail price (based on Apple’s pricing).

The Price of a Byte and all that Jazz

So how does the above data-price plans look like in terms of Price-per-Giga-Byte?

Although in most cases not be very clear to the consumer, the data-centric price plan is structured around the price of the primary data allowance (i.e., the variable part) and non-data related bundled services included in the plan (i.e., the fixed service part representing non-data items).

There will be a variable price reflecting the data-centric price-plans data allowance and a “Fixed” Service Fee that capture the price of bundled services such as voice and SMS. Based on total price of the data-centric price plan, it will often appear that the higher the allowance the cheaper does your unit-data “consumption” (or allowance) become. Indicating that volume discounts have been factored into the price-plan. In other words, the higher the data allowance the lower the price per GB allowance.

This is often flawed logic and simply an artefact of the bundled non-data related services being priced into the plan. However, to get to that level of understanding requires a bit of analysis that most of us certainly don’t do before a purchase.

- Figure above: Illustrates the unit-price of a Giga Byte (GB) versus AA’s various data-centric price plans. Note the price plans can be decomposed into a variable data-usage attributable price (per GB) and a fixed service fee that accounts for non-data services blended into the price. The Data Consumption per GB is the variable data-usage dependable part of the Price Plan and the Total price per GB is the full price normalized to the plans data consumption allowance.

So with the above we have argued that the total data-centric price can be written as a fixed and a variable part;

As will be described in more detail below, the data-centric price

The “Fixed Service Fee” depends on all the non-data related goodies that are added to the data-centric price plan, such as (a) unlimited voice, (b) unlimited SMS, (c) Price plan applies Europe-wide (i.e., EU-Option), (d) handset subsidy recovery fee, (e) maybe a customer management fee, etc..

For most price data-centric plan, If the data-centric price divided by the allowance would be plotted against the allowance

- Figure above: illustration of the data-centric pricing on a per GB level plotted versus the GB allowance. Source: Dr. Kim K Larsen’s Mind Share contribution at Informa’s LTE World Summit May 2012; “Right pricing LTE and mobile broadband in general (a Technologist’ Observations”.

Nothing really surprising given the pricing math involved! It is instructive to see what actually happens when we take a data-centric price and divide by the corresponding data allowance;

For very large data allowances

We can also observe that If the total price, of a data-centric price plan associated with a given data allowance (i.e., GB), is used to derive a price-per-GB, one would conclude that most mobile operators provide the consumer with volume discounts as they adapt higher data allowance plans. The GB gets progressively cheaper for higher usage plans. As most data-centric price plans are in the range where

It is clear that data-allowance normalizing the totality of a data-centric price plan, particular when non-data services have been blended into the plan, will not reveal the real price of data. If used for assessing, for example, data profitability or other mobile data related financial KPIs this approach might be of very little use.

- Figure above: illustrates the basic characteristics of a data-centric price plan normalized by the data allowance. The data for this example reflects the AA’s data-centric price plans 2x4G Speed with bundled unlimited Voice & SMS as well as applying EU-wide. We see that the Beta value corresponds to a Volume Discount (at values lower than 1) or a Volume Penalty (at values higher than 1).

Oh yeah! … The really “funny” part of most data-price plan analysis (including my own past ones!) are they are more likely to reflect the Fixed Service Part (independent of the Data allowance) of the Data-centric price plan than the actual unit price of mobile data.

What to expect from AA’s data-centric price plans?

so in a rational world of data-centric pricing (assuming such exist) what should we expect of Anything Anywhere’s price plans as advertised online;

- The (embedded) price for unlimited voice would be the same irrespective of the data plan’s allowed data usage (i.e., unlimited Voice does not depend on data plan).

- The (embedded) price for unlimited SMS would be the same irrespective of the data plan’s allowed data usage (i.e., unlimited SMS does not depend on data plan).

- You would pay more for having your plan extended to apply across Europe Union compared to not having this option.

- You would (actually you should) expect to pay more per Mega Byte for the Double Speed option as compared to the Single Speed Option.

- If you decide to “finance” your handset purchase (i.e., pay less upfront option) within a data plan you should expect to pay more on a monthly basis.

- Given a data plan has a whole range of associated handsets priced From Free (i.e., included in plan without extra upfront charge) to high-end high-priced Smartphones, such as iPhone 6 Plus 128 GB, you would not expect that handset related cost would have been priced into the data plan. Or if it is, it must be the lowest common denominator for the whole range of offered handsets at a given price plan.

- Where the discussion becomes really interesting is how your data consumption should be priced; (1) You pay more per unit of data consumption as you consume more data on a monthly basis, (2) You pay the same per unit irrespective of your consumption or (3) You should have a volume discount making your units cheaper the more you consume.

of course the above is if and only if the price plans have been developed in reasonable self-consistent manner.

- Figure above: Illustrates AA’s various data-centric price plans (taken from their web site). Note that PPM represents low upfront (terminal) cost for the consumer and higher monthly cost and PUF represent paying upfront for the handset and thus having lower monthly costs as a consequence. The Operator AA allows the consumer in the PPM Plan to choose for an iPhone 6 Plus 128GB (priced at 100 to 160) or an IPhone 6 Plus 64GB option (at a lower price of course).

First note that Price Plans (with more than 2 data points) tend to be linear with the Data Usage allowance.

The Fixed Service Fee – The Art of Re-Capture Lost legacy Value?

In the following I define the Fixed Service Fee as the part of the total data-centric price plan that is independent of a given plan’s data allowance. The logic is that this part would contain all non-data related cost such as Unlimited Voice, Unlimited SMS, EU-Option, etc..

From AA’s voice plan (for 250 Minutes @ 10 per Month & 750 Minutes @ 15 per Month) with unlimited SMS (& no data) it can be inferred that

- Price of Unlimited SMS can be no higher than 7.5. This however is likely also include general customer maintenance cost.

Monthly customer maintenance cost (cost of billing, storage, customer care & systems support, etc.) might be deduced from the SIM-Only Data-Only package and would be

- Price of Monthly Customer Maintenance could be in the order of 5, which would imply that the Unlimited SMS price would be 2.5. Note the market average Postpaid SMS ARPU in 2014 was ca., 8.40 (based on Pyramid Research data). The market average number of postpaid SMS per month was ca. 273 SMS.

From AA’s SIM-only plan we get that the fixed portion of providing service (i.e., customer maintenance, unlimited Voice & SMS usage) is 14 and thus

- Price of Unlimited Voice should be approximately 6.5. Note the market average Postpaid Voice ARPU was ca. 12 (based on Pyramid Research data). The market average voice usage per month was ca. 337 minutes. Further from the available limited voice price plans it can be deduced that unlimited voice must be higher than 1,000 Minutes or more than 3 times the national postpaid average.

The fixed part of the data-centric pricing difference between the data-centric SIM-only plan and similar data-centric plan including a handset (i.e., all services are the same except for the addition of the handset) could be regarded as a minimum handset financing cost allowing the operator to recover some of the handset subsidy

- Equipment subsidy recovery cost of 7 (i.e., over a 24 month period this amounts to 168 which is likely to recover the average handset subsidy). Note is the customer chooses to pay little upfront for the handset, the customer would have to pay 26 extra per month in he fixed service fee. Thus low upfront cost result in another 624 over the 24 month contract period. Interestingly is that with the initial 7 for handset subsidy recovery in the basic fixed service fee a customer would have paid 792 in handset recovery over 24 month period the contract applies to (a bit more than the iPhone 6 Plus 128GB retail price).

The price for allowing the data-centric price-plan to apply Europe Union Wide is

- The EU-Option (i.e., plan applicable within EU) appears to be priced at ca. 5 (caution: 2x4G vis-a-vis 1x4G could have been priced into this delta as well).

For EU-option price it should be noted here that the two plans that are being compared differs not only in the EU-option. The plan without the EU option is a data plan with “normal” 4G speed, while the EU-option plan supports double 4G speeds. So in theory the additional EU-option charge of 5 could also include a surcharge for the additional speed.

Why an operator would add the double speed to the fixed Service Fee price part is “bit” strange. The 2x4G speed price-plan option clearly is a variable trigger for cost (and value to the customer’s data usage). Thus should be introduced in the the variable part (i.e., the Giga-Byte dependent part) of the data-centric price plan.

It is assumed that indeed the derived difference can be attributed to the EU-option, i.e., the double speed has not been include in the monthly Fixed Service Fee.

In summary we get AA’s data-centric price plan’s monthly Fixed Service Fee de-composition as follows;

- Figure above: shows the composition of the monthly fixed service fee as part of AA’s data-centric plans. Of course in a SIM-only scenario the consumer would not have the Handset Recovery Fee inserted in the price plan.

So irrespective of the data allowance a (postpaid) customer would pay between 26 to 52 per month depending on whether handset financing is chosen (i.e., Low upfront payment on the expense of higher monthly cost).

Mobile data usage still has to happen!

The price of Mobile Data Allowance.

The variable data-price in the studied date-centric price plans are summarized in the table below as well as the figure;

Price-plan |

4G Speed |

Price per GB |

|

Pay Less Upfront More per Month |

Double |

0.61±0.03 |

|

Pay Upfront & Less per Month |

Double |

0.67±0.05 |

|

SIM-Only |

Single |

1.47±0.08 |

|

SIM-Only Data Only |

Single |

2 (only 2 data points) |

The first thing that obviously should make you Stop in Wonder is that Single 4G Speed Giga Byte is more than Twice the price of a Double 4G Speed Giga Byte … In need for speed … well that will give you a pretty good deal with AA’s price 2x4G plans.

Second thing to notice is that it would appear to be a really bad deal (with respect to the price-per-byte) to be a SIM-Only Data-Only customer.

The Data-Only pays 2 per GB. Almost 3 times more than if you would choose a subscription with a device, double speed, double unlimited and EU-wide applicable price plan.

Agreed! In absolute terms the SIM-only Data-only cost a lot less per month (9 less than the 20GB pay device upfront) and it is possible to run away after 12 months (versus the 24 month plans). One rationale for charging extra per Byte for a SIM-only Data-only plan could be that the SIM card might be used in Tablet or Data-card/Dongle products that typically does consume most if not all of a given plans allowance. For normal devices and high allowance plans on average the consumption can be quiet a lot lower than the actual allowance. Particular over a 24 month period.

You might argue that this is all about how the data-centric price plans have been de-composed in a fixed service fee (supposedly the non-data dependent component) and a data consumptive price. However, even when considering the full price of a given price plan is the Single-4G-Speed more expensive per Byte than Double-4G-Speed.

You may also argue that I am comparing apples and oranges (or even bananas pending taste) as the Double-4G-Speed plans include a devices and a price-plan that applies EU-wide versus the SIM-only plan that includes the customers own device and a price-plan that only works in United. All true of course … Why that should be more expensive to opt out of is a bit beyond me and why this should have an inflationary impact on the price-per-Byte … well a bit of a mystery as well.

At least there is no (statistical) difference in the variable price of a Giga Byte whether the customer chooses to pay of her device over the 24 month contract period or pay (most of) it upfront.

For AA it doesn’t seem to be of concern! …. As 88% would come back for more (according with their web site).

Obviously this whole analysis above make the big assumption that the data-centric price plans are somewhat rationally derived … this might not be the case!

and it assumes that rationally & transparently derived price plans are the best for the consumer …

and it assumes what is good for the consumer is also good for the company …

Is AA different in this respect to that of other Operators around the world …

No! AA is not different from any other incumbent operator coming from a mobile voice centric domain!

Acknowledgement

I greatly acknowledge my wife Eva Varadi for her support, patience and understanding during the creative process of creating this Blog.

Postscript – The way I like to look at (rational … what ever that means) data-centric pricing.

Firstly, it would appear that AA’s pricing philosophy follows the industry standard of pricing mobile services and in particular mobile data-centric services by the data volume allowance. Non-data services are added to the data-centric price plan and in all effect make up for the most part of the price-plan even at relative higher data allowances;

- Figure above: illustrates the typical approach to price plan design in the Telecom’s industry. Note while not per se wrong it often overweight’s the volume element of pricing and often results in sub-optimizing the Quality and Product aspects . Source: Dr. Kim K Larsen’s Mind Share contribution at Informa’s LTE World Summit May 2012; “Right pricing LTE and mobile broadband in general (a Technologist’ Observations)”.

Unlimited Voice and SMS in AA’s standard data-centric plans clearly should mitigate possible loss or migration away from old fashion voice (i.e., circuit switched) and SMS. However both the estimated allowances for unlimited voice (6.5) and SMS (2.5) appear to be a lot lower than their classical standalone ARPUs for the postpaid category. This certainly could explain that this market (as many others in Western Europe) have lost massive amount of voice revenues over the last 5 years. In other words re-capturing or re-balancing legacy service revenues into data-centric plans still have some way to go in order to be truly effective (if at all possible which is highly questionable at this time and age).

- Figure above: illustration of what to consider when pricing a product or developing a pricing plan. The figure is based on H.E Homa’s wonderful notes on “Pricing Fundamentals”. Source: Dr. Kim K Larsen’s Mind Share contribution at Informa’s LTE World Summit May 2012; “Right pricing LTE and mobile broadband in general (a Technologist’ Observations”. It should be noted that the above is very much driven from the point of view of value-based pricing. It is an inherent assumption Value-to-Customer (VtP) is also consistent with the consumer’s Willingness to Pay (WtP).

As a Technologist, I am particular interested in how the technology cost and benefits are being considered in data-centric price plans.

The big challenge for the pricing expert who focus too much on volume is that the same volume can result from vastly different network qualities and speed. The customers handset will drive the experience of quality and certainly consumption. By that differences in network load and thus technology cost. A customer with a iPhone 6 Plus is likely to load the mobile data network more (and thus incur higher cost) than a customer with a normal screen smartphone of 1 or 2 generations removed from iPhone 6 Plus. It is even conceivable that a user with iPhone 6 Plus will load the network more than a customer with a normal iPhone 6 (independent of the iOS). This is very very different for Voice and SMS volumetric considerations in legacy price plans, where handset had little (or no) impact on network load relative to the usage.

For data-centric price plans to be consistent with the technology cost incurred one should consider;

- Higher “guarantied” Quality, typically speed or latency, should be priced higher per Byte than lower quality plans (or at the very least not lower).

- Higher Volumetric Allowances should be priced per Byte higher than Lower Volumetric Allowance (or at the very least not lower).

- Offering unlimited Voice & SMS in data-centric plans (as well as other bundled goodies) should be carefully re-balanced to re-capture some of lost legacy revenues.

That AA’s data-centric plans for double speed appears to be cheaper than their plans at a lower data delivery quality level is not consistent with costing. Of course, AA cannot really guaranty that the customer will get double 4G speed everywhere and as such it may not be fair to charge substantially more than for single speed. However, this is of course not what appear to happen here.

AA’s lowest data unit price (in per Giga Byte) is around 0.6 – 0.7 (or 0.06 – 0.07 Cent per Mega Byte). That price is very low and in all likelihood lower than their actual production cost of a GB or MB.

However, one may argue that as long as the Total Service Revenue gained by a data-centric price plan recover the production cost, as well as providing a healthy margin then whether the applied data unit-price is designed to recover the data production cost is maybe less of an issue.

In other words, data profitability may not matter as much as overall profitability. This said it remains in my opinion in-excusable for a mobile operator not to understand its main (data) cost drivers and ensure it is recovered in their overall pricing strategies.

Surely! You may say? … “Surely Mobile Operators know their cost structure and respective cost drivers and their price plans reflects this knowledge?”

It is my observation that most price plans (data-centric or not) are developed primarily in response to competition (which of course is an important pricing element as well) rather than firmly anchored in Cost, Value & Profit considerations. Do Operators really & deeply know their own cost structure and cost drivers? … Ahhh … In my opinion few really appear to do!