How to think about a single network future? What does it entail, and what is it good for?

Well, imagine a world where your mobile device, unchanged and unmodified, connects to the nearest cell tower and satellites orbiting Earth, ensuring customers will always be best connected, getting the best service, irrespective of where they are. Satellite-based supplementary coverage (from space) seeks to deliver on this vision by leveraging superior economic coverage in terms of larger footprint (than feasible with terrestrial networks) and better latency (compared to geostationary satellite solutions) to bring connectivity directly to unmodified consumer handsets (e.g., smartphone, tablet, IoT devices), enhance emergency communication, and foster advancements in space-based technologies. The single network future does not only require certain technological developments, such as 3GPP Non-Terrestrial Network standardization efforts (e.g., Release 17 and forward). We also need the regulatory spectrum policy to change, allowing today’s terrestrially- and regulatory-bounded cellular frequency spectra to be re-used by satellite operators providing the same mobile service under satellite coverage in areas without terrestrial communications infrastructure, as mobile customers enjoy within the normal terrestrial cellular network.

It is estimated that less than 40% of the world’s population, or roughly 2.9 billion people, have never used the internet (as of 2023). That 60% of the world population have access to internet and 40% have not, is the digital divide. A massive gap most pronounced in developing countries, rural & remote areas, and among older populations and economically disadvantaged groups. Most of the 2.9 billion on the wrong side of the divide live in areas lacking terrestrial-based technology infrastructure that would readily facilitate access to the internet. It lacks the communications infrastructure because it may either be impractical or (and) un-economical to deploy, including difficulty in monetizing and yielding a positive return on investment over a relatively short period. Satellites that are allowed by regulatory means to re-use terrestrially-based cellular spectrum for supplementary (to terrestrial) coverage can largely solve the digital divide challenges (as long as affordable mobile devices and services are available to the unconnected).

This blog explores some of the details of the, in my opinion, forward-thinking FCC’s Supplementary Coverage from Space (SCS) framework and vision of a Single Network in which mobile cellular communication is not limited to tera firma but supplemented and enhanced by satellites, ensuring connectivity everywhere.

SUPPLEMENTARY COVERAGE FROM SPACE.

Federal Communications Commission (FCC) recently published a new regulatory framework (“Report & Order and further notice of proposed rulemaking“) designed to facilitate the integration of satellite and terrestrial networks to provide Supplemental Coverage from Space (SCS), marking a significant development toward achieving ubiquitous connectivity. In the following, I will use the terms “SCS framework” and ” SCS initiative” to cover the reference to the FCC’s regulatory framework. The SCS initiative, which, to my knowledge, is the first of its kind globally, aims to allow satellite operators and terrestrial service providers to collaborate, leveraging the spectrum previously allocated exclusively for terrestrial services to extend connectivity directly to consumer handsets, what is called satellite direct-to-device (D2D), especially in remote, unserved, and underserved areas. The proposal is expected to enhance emergency communication availability, foster advancements in space-based technologies, and promote the innovative and efficient use of spectrum resources.

The “Report and Order” formalizes a spectrum-use framework, adopting a secondary mobile-satellite service (MSS) allocation in specific frequency bands devoid of primary non-flexible-use legacy incumbents, both federal and non-federal. Let us break this down in a bit more informal language. So, the FCC proposes to designate certain parts of the radio frequency spectrum (see below) for mobile-satellite services on a “secondary” basis. In spectrum management, an allocation is deemed “secondary” when it allows for the operation of a service without causing interference to the “primary” services in the same band. This means that the supplementary satellite service, deemed secondary, must accept interference from primary services without claiming protection. Moreover, this only applies to locations that lack (i.e., devoid of) the use of a given frequency band by existing ” primary” spectrum users (i.e., incumbents), non-federal as well as federal primary uses.

The setup encourages collaboration and permits supplemental coverage from space (SCS) in designated bands where terrestrial licensees, holding all licenses for a channel throughout a geographically independent area (GIA), lease access to their terrestrial spectrum rights to a satellite operator. Furthermore, the framework establishes entry criteria for satellite operators to apply for or modify an existing “part 25” space station license for SCS operations, that is the regulatory requirements established by the FCC governing the licensing and operation of satellite communications in the United States. The framework also outlines a licensing-by-rule approach for terrestrial devices acting as SCS earth stations, referring to a regulatory and technological framework where conventional consumer devices, such as smartphones or tablets, are equipped to communicate directly with satellites (after all we do talk about Direct-2-Device).

Additionally, the Further Notice of Proposed Rulemaking seeks further commentary on aspects such as 911 service provision and the protection of radio astronomy, indicating the FCC’s consistent commitment to refining and expanding the SCS framework responsibly. This commitment ensures that the framework will continue to evolve, adapting to new challenges and opportunities and providing a solid foundation for future developments.

BALANCING THE AIRWAVES IN THE USA.

Two agencies in the US manage the frequency spectrum, the Federal Communications Commission (FCC) and the National Telecommunications and Information Administration (NTIA) . They collaboratively manage and coordinate frequency spectrum use and reuse for satellites, among other applications, within the United States. This partnership is important for maintaining a balanced approach to spectrum management that supports federal and non-federal needs, ensuring that satellite communications and other services can operate effectively without causing harmful interference to each other.

The Federal Communications Commission, the FCC for short, is an independent agency that exclusively regulates all non-Federal spectrum use across the United States. FCC allocates spectrum licenses for commercial use, typically through spectrum auctions. A new or re-purposed commercialized spectrum has been reclaimed from other uses, both from federal uses and existing commercial uses. Spectrum can be re-purposed either because newer, more spectrally efficient technologies become available (e.g., the transition from analog to digital broadcasting) or it becomes viable to shift operation to other spectrum bands with less commercial value (and, of course, without jeopardizing existing operational excellence). It is also possible that spectrum, previously having been for exclusive federal use (e.g., military applications, fixed satellite uses, etc.), can be shared, such as the case with Citizens Broadband Radio Service (CBRS), which allows non-federal parties access to 150 MHz in the 3.5 GHz band (i.e., band 48). However, it has recently been concluded that (centralized) dynamic spectrum sharing only works in certain use cases and is associated with considerable implementation complexities. Multiple parties with possible vastly different requirements co-exist within a given band, which is a work in progress and may not be consistent with the commercialized spectrum operation required for high-quality broadband cellular operation.

Alongside the FCC, the National Telecommunications and Information Administration (NTIA) plays a crucial role in US spectrum management. The NTIA is the sole authority responsible for authorizing Federal spectrum use. It also serves as the principal adviser on telecommunications policies to the President of the United States, coordinating the views of the Executive Branch. The NTIA manages a significant portion of the spectrum, approximately 2,398 MHz (69%), within the range of 225 MHz to 3.7 GHz, known as the ‘beachfront spectrum’. Of the total 3,475 MHz, 591 MHz (17%) is exclusively for Federal use, and 1,807 MHz (52%) is shared or coordinated between Federal and non-Federal entities. This leaves 1,077 MHz (31%) for exclusive commercial use, which falls under the management of the FCC.

NTIA, in collaboration with the FCC, has been instrumental in the past in freeing up substantial C-band spectrum, 480 MHz in total, of which 100 MHz is conditioned on prioritized sharing (i.e., Auction 105), for commercial and shared use that subsequently has been auctioned off over the last three years raising USD 109 billion. In US Dollar (USD) per MHz per population count (pop), we have, on average, ca. USD 0.68 per MHz-pop from the C-band auctions in the US, compared to USD 0.13 per MHz-pop in Europe C-band auctions and USD 0.23 per MHz-pop in APAC auctions. It should be remembered that the United States exclusive-use spectrum licenses can be regarded as an indefinite-lived intangible asset, while European spectrum rights expire between 10 and 20 years. This may explain a big part of the difference between US-based spectrum pricing and Europe and Asia.

The FCC and the NTIA jointly manage all the radio spectrum in the United States, licensed (e.g., cellular mobile frequencies, TV signals) and unlicensed (e.g., WiFi, MW Owens). The NTIA oversees spectrum use for Federal purposes, while the FCC is responsible for non-Federal use. In addition to its role in auctioning spectrum licenses, the FCC is also authorized to redistribute licenses. This authority allows the FCC to play a vital role in ensuring efficient spectrum use and adapting to changing needs.

THE SINGLE NETWORK.

The Supplementary Coverage from Space (SCS) framework creates an enabling regulatory framework for satellite operators to provide mobile broadband services to unmodified mobile devices (i.e., D2D services), such as smartphones and other terrestrial cellular devices, in rural and remote areas without such services, where no or only scarce terrestrial infrastructure exists. By leveraging SCS, terrestrial cellular broadband services will be enhanced, and the combination may result in a unified network. This network will ensure continuous and ubiquitous access to communication services, overcoming geographical and environmental challenges. Thus, this led to the inception of the Single Network that can provide seamless connectivity across diverse environments, including remote, unserved, and underserved areas.

How does the “Single Network” of FCC differ from the 3GPP Non-Terrestrial Network (NTN) standardization? Simply put, the “Single Network” is a regulatory framework that paves the way for satellite operators to re-use the terrestrial cellular spectrum on their non-terrestrial (satellite-based) network. The 3GPP NTN standardization initiatives, e.g., Release 16, 17 and 18+, are a technical effort to incorporate satellite communication systems within the 5G network architecture. Shortly, the following 3GPP releases are it relates to how NTN should function with terrestrial 5G networks;

- Release 15 laid the groundwork for 5G New Radio (NR) and started to consider the broader picture of integrating non-terrestrial networks with terrestrial 5G networks. It marks the beginning of discussions on how to accommodate NTNs within the 5G framework, focusing on study items rather than specific NTN standards.

- Release 16 took significant steps toward defining NTN by including study items and work items specifically aimed at understanding and specifying the adjustments needed for NR to support communication with devices served by NTNs. Release 16 focuses on identifying modifications to the NR protocol and architecture to accommodate the unique characteristics of satellite communication, such as higher latency and different mobility characteristics compared to terrestrial networks.

- Release 17 further advancements in NTN specifications aiming to integrate specific technical solutions and standards for NTNs within the 5G architecture. This effort includes detailed specifications for supporting direct connectivity between 5G devices and satellites, covering aspects like signal timing, frequency bands, and protocol adaptations to handle the distinct challenges posed by satellite communication, such as the Doppler effect and signal delay.

- Release 18 and beyond will continue to evolve its standards to enhance NTN support, addressing emerging requirements and incorporating feedback from early implementations. These efforts include refining and expanding NTN capabilities to support a broader range of applications and services, improving integration with terrestrial networks, and enhancing performance and reliability.

The NTN architecture ensures (should ensure) that satellite communications systems can seamlessly integrate into 5G networks, supporting direct communication between satellites and standard mobile devices. This integration idea includes adapting 5G protocols and technologies to accommodate the unique characteristics of satellite communication, such as higher latency and different signal propagation conditions. The NTN standardization aims to expand the reach of 5G services to global scales, including maritime, aerial, and sparsely populated land areas, thereby aligning with the broader goal of universal service coverage.

The FCC’s vision of a “single network” and the 3GPP NTN standardization aims to integrate satellite and terrestrial networks to extend connectivity, albeit from slightly different angles. The FCC’s concept provides a regulatory and policy framework to enable such integration across different network types and service providers, focusing on the broad goal of universal connectivity. In contrast, 3GPP’s NTN standardization provides the technical specifications and protocols to make this integration possible, particularly within next-generation (5G) networks. At the same time, 3GPP’s NTN efforts address the technical underpinnings required to realize that vision in practice, especially for 5G technologies. The FCC’s “single network” concept lays the regulatory foundation for enabling satellite and terrestrial cellular network service integration to the same unmodified device portfolio. Together, they are highly synergistic, addressing the regulatory and technical challenges of creating a seamlessly connected world.

SINGLE NETWORK VS SATELLITE ATC

The FCC’s Single Network vision and the Supplemental Coverage from Space (SCS) concept, akin to the Satellite Ancillary Terrestrial Component (ATC) architectural concept (an area that I spend a significant portion of my career working on operationalizing and then defending … a different story though), share a common goal of merging satellite and terrestrial networks to fortify connectivity. These strategies, driven by the desire to enhance the reach and reliability of communication services, particularly in underserved regions, hold the promise of expanded service coverage.

The Single Network and SCS initiatives broadly focus on comprehensively integrating satellite services with terrestrial infrastructures, aiming to directly connect satellite systems with standard consumer devices across various services and frequency bands. This expansive approach seeks to ensure ubiquitous connectivity, significantly closing the coverage gaps in current network deployments. Conversely, the Satellite ATC concept is more narrowly tailored, concentrating on using terrestrial base stations to complement and enhance satellite mobile services. This method explicitly addresses the need for improved signal availability and service reliability in urban or obstructed areas by integrating terrestrial components within the satellite network framework.

Although the Single Network and Satellite ATC shared goals, the paths to achieving them diverge significantly in the application, regulatory considerations, and technical execution. The SCS concept, for instance, involves navigating regulatory challenges associated with direct-to-device satellite communications, including the complexities of spectrum sharing and ensuring the harmonious coexistence of satellite and terrestrial services. This highlights the intricate nature of network integration, making your audience more aware of the regulatory and technical hurdles in this field.

The distinction between the two concepts lies in their technological and implementation specifics, regulatory backdrop, and focus areas. While both aim to weave together the strengths of satellite and terrestrial technologies, the Single Network and SCS framework envisions a more holistic integration of connectivity solutions, contrasting with the ATC’s targeted approach to augmenting satellite services with terrestrial network support. This illustrates the evolving landscape of communication networks, where the convergence of diverse technologies opens new avenues for achieving seamless and widespread connectivity.

THE RELATED SCS FREQUENCIES & SPECTRUM.

The following frequency bands and the total bandwidth associated with the frequency have by the FCC been designated for Supplemental Coverage from Space (SCS):

- 70MHz @ 600 MHz Band

- 96 MHz @ 700 MHz Band

- 50 MHz @ 800 MHz Band

- 130 MHz @ Broadband PCS

- 10 MHz @ AWS-H Block

The above comprises a total frequency bandwidth of 350+ MHz, currently used for terrestrial cellular services across the USA. According to the FCC, the above frequency bands and spectrum can also be used for satellite direct-to-device SCS services to normal mobile devices without built-in satellite transceiver functionality. Of course, this is subject to spectrum owners’ approval and contractual and commercial arrangements.

Moreover, the 758-769/788-799 MHz band, licensed to the First Responder Network Authority (FirstNet), is also eligible for SCS under the established framework. This frequency band has been selected to enhance connectivity in remote, unserved, and underserved areas by facilitating collaborations between satellite and terrestrial networks within these specific frequency ranges.

SpaceX recently reported a peak download speed of 17 Mb/s from a satellite direct to an unmodified Samsung Android Phone using 2×5 MHz of T-Mobile USA’s PCS (i.e., the G-block). The speed corresponds to a downlink spectral efficiency of ~3.4 Mbps/MHz/beam, which is pretty impressive. Using this as rough guidance for the ~350 MHz, we should expect this to be equivalent to an approximate download speed of ca. 600 Mbps (@ 175 MHz) per satellite beam. As the satellite antenna technology improves, we should expect that spectral efficiency will also increase, resulting in increasing downlink throughput.

SCS INFANCY, BUT ALIVE AND KICKING.

In the FCC’s framework on the Supplemental Coverage from Space (SCS), the partnership between SpaceX and T-Mobile is described as a collaborative effort where SpaceX would utilize a block of T-Mobile’s mid-band Personal Communications Services (PCS G-Block) spectrum across a nationwide footprint. This initiative aims to provide service to T-Mobile’s subscribers in rural and remote locations, thereby addressing coverage gaps in T-Mobile’s terrestrial network. The FCC has facilitated this collaboration by allowing SpaceX and T-Mobile to deploy and test their proposed SCS system while their pending applications and the FCC’s proceedings continue.

Specifically, SpaceX has been authorized (by FCC’s Space Bureau) to deploy a modified version of its second-generation (2nd generation) Starlink satellites with SCS-capable antennas that can operate in specific frequencies. FCC authorized experimental testing on terrestrial locations for SpaceX and T-Mobile to progress with their SCS system, although SpaceX’s requests for broader authority remain under consideration by the FCC.

Lynk Global has partnered with mobile network operators (MNOs) outside the United States to allow the MNOs’ customers to send texts using Lynk’s satellite network. In 2022, the FCC authorized Lynk’s request to operate a non-geostationary satellite orbit (NGSO) satellite system (e.g., Low-Earth Orbit, Medium Earth Orbit, or Highly-Elliptical Orbit) intended for text message communications in locations outside the United States and in countries where Lynk has obtained agreements with MNOs and the required local regulatory approval. Lynk aims to deploy ten mobile-satellite service (MSS) satellites as part of a “cellular-based satellite communications network” operating on cellular frequencies globally in the 617-960 MHz band (i.e., within the UHF band), targeting international markets only.

Lynk has announced contracts with more than 30 MNOs (full list not published) covering over 50 countries for Lynk’s “satellite-direct-to-standard-mobile-phone-system,” which provides emergency alerts and two-way Short Message Service (SMS) messaging. Lynk currently has three LEO satellites in orbit as of March 2023, and they plan to expand their constellation to include up to 5,000 satellites with 50 additional satellites planned for end of 2024, and with that substantially broadening its geographic coverage and service capabilities. Lynk recently claimed that they had in Hawaii achieved repeated successful downlink speeds above 10 Mbps with several mass market unmodified smartphones (10+ Mbps indicates a spectral efficiency of 2+ Mbps/MHz/beam). Lynk Mobile has also, recently (July 2023) demonstrated (as a proof of concept) phone calls via their LEO satellite between two unmodified smartphones (see the YouTube link).

AST SpaceMobile is also mentioned for its partnerships with several MNOs, including AT&T and Vodafone, to develop its direct-to-device or satellite-to-smartphone service. Overall AST SpaceMobile has announced it has entered into “more than 40 agreements and understandings with mobile network operators globally” (e.g., AT&T, Vodafone, Rakuten, Orange, Telefonica, TIM, MTN, Ooredoo, …). In 2020, AST filed applications with the FCC seeking U.S. market access for gateway links in the V-band for its SpaceMobile satellite system, which is planned to consist of 243 LEO satellites. AST clarified that its operation in the United States would collaborate with terrestrial licensee partners without seeking to operate independently on terrestrial frequencies.

AST SpaceMobile’s satellite antenna design marks a pioneering step in satellite communications. AST recently deployed the largest commercial phased array antenna into Low Earth Orbit (LEO). On September 10, 2022, AST SpaceMobile launched its prototype direct-to-device testbed BlueWalker 3 (BW3) satellite. This mission marked a significant step forward in the company’s efforts to test and validate its technology for providing direct-to-cellphone communication via a Low Earth Orbit (LEO) satellite network. The launch of BW3 aimed to demonstrate the capabilities of its large phased array antenna, a critical component for the AST’s targeted global broadband service.

The BW3’s phased array antenna with a surface area of 64 square meters is technologically quite advanced (actually, I find it very beautiful and can’t wait to see the real thing for their commercial constellation) and designed for dynamic beamforming as one would expect for a state-of-art direct-to-device satellite. The BlueWalker 3, a proof of concept design, supports a frequency range of 100 MHz in the UHF band, with 5 MHz channels and a spectral efficiency expected to be 3 Mbps/MHz/channel. This capability is crucial for establishing direct-to-device communications, as it allows the satellite to concentrate its signals on specific geographic areas or directly on mobile devices, enhancing the quality of coverage and minimizing potential interference with terrestrial networks. AST SpaceMobile is expected to launch the first 5 of 243 LEO satellites, BlueBirds, on SpaceX’s Falcon 9 in the 2nd quarter of 2024. The first 5 will be similar to BW3 design including the phased array antenna. Subsequent AST satellites are expected to be larger with substantially up-scaled phased array antenna supporting an even larger frequency span covering the most of the UHF band and supporting 40 MHz channels with peak download speeds of 120 Mbps (using their estimated 3 Mbps/MHz/channel).

These above examples underscore the the ongoing efforts and potential of satellite service providers like Starlink/SpaceX, Lynk Global, and AST SpaceMobile within the evolving SCS framework. The examples highlight the collaborative approach between satellite operators and terrestrial service providers to achieve ubiquitous connectivity directly to unmodified cellular consumer handsets.

PRACTICAL PREREQUISITES.

In general, the satellite operator would need a terrestrial frequency license owner willing to lease out its spectrum for services in areas where that spectrum has not been deployed on its network infrastructure or where the license holder has no infrastructure deployed. And, of course, a terrestrial communication service provider owning spectrum and interested in extending services to remote areas would need a satellite operator to provide direct-to-device services to its customers. Eventually, terrestrial operators might see an economic benefit in decommissioning uneconomical rural terrestrial infrastructure and providing satellite broadband cellular services instead. This may be particularly interesting in low-density rural and remote areas supported today by a terrestrial communications infrastructure.

Under the SCS framework, terrestrial spectrum owners can make leasing arrangements with satellite operators. These agreements would allow satellite services to utilize the terrestrial cellular spectrum for direct satellite communication with devices, effectively filling coverage gaps with satellite signals. This kind of arrangement could be similar to the one between T-Mobile USA and StarLink to offer cellular services in the absence of T-Mobile cellular infrastructure, e.g., mainly remote and rural areas.

As the regulatory body for non-federal frequencies, the FCC delineates a regulatory environment that specifies the conditions under which the spectrum can be shared or used by terrestrial and satellite services, minimizing the risk of harmful interference (which both parties should be interested in anyway). This includes setting technical standards and identifying suitable frequency bands supporting dual use. The overarching goal is to bolster the reach and reliability of cellular networks in remote areas, enhancing service availability.

For terrestrial cellular networks and spectrum owners, this means adhering to FCC regulations that govern these new leasing arrangements and the technical criteria designed to protect incumbent services from interference. The process involves meticulous planning and, if necessary, implementing measures to mitigate interference, ensuring that the integration of satellite and terrestrial networks proceeds smoothly.

Moreover, the SCS framework should leapfrog innovation and allow network operators to broaden their service offerings into areas where they are not present today. This could include new applications, from emergency communications facilitated by satellite connectivity to IoT deployments and broadband access in underserved locations.

TECHNICAL PREREQUISITES FOR DELIVERING SATELLITE SCS SERVICES.

Satellite constellations providing D2D services are naturally targeting supplementary coverage of geographical areas where no terrestrial cellular services are present at the target frequency bands used by the satellite operator.

As the satellite operator has gotten access to the terrestrial cellular spectrum for its supplementary coverage direct-to-device service, it has a range of satellite technical requirements that either need to be in place of an existing constellation (though that might require some degree of foresight) or a new satellite would need to be designed consistent with frequency band and range, the targeted radio access technology such as LTE or 5G (assuming the ambition eventually is beyond messaging), and the device portfolio that the service aims to support (e.g., smartphone, tablet, IoTs, …). In general, I would assume that existing satellite constellations would not automatically support SCS services they have not been designed for upfront. It would make sense (economically) if a spectrum arrangement already exists between the satellite and terrestrial cellular spectrum owner and operator.

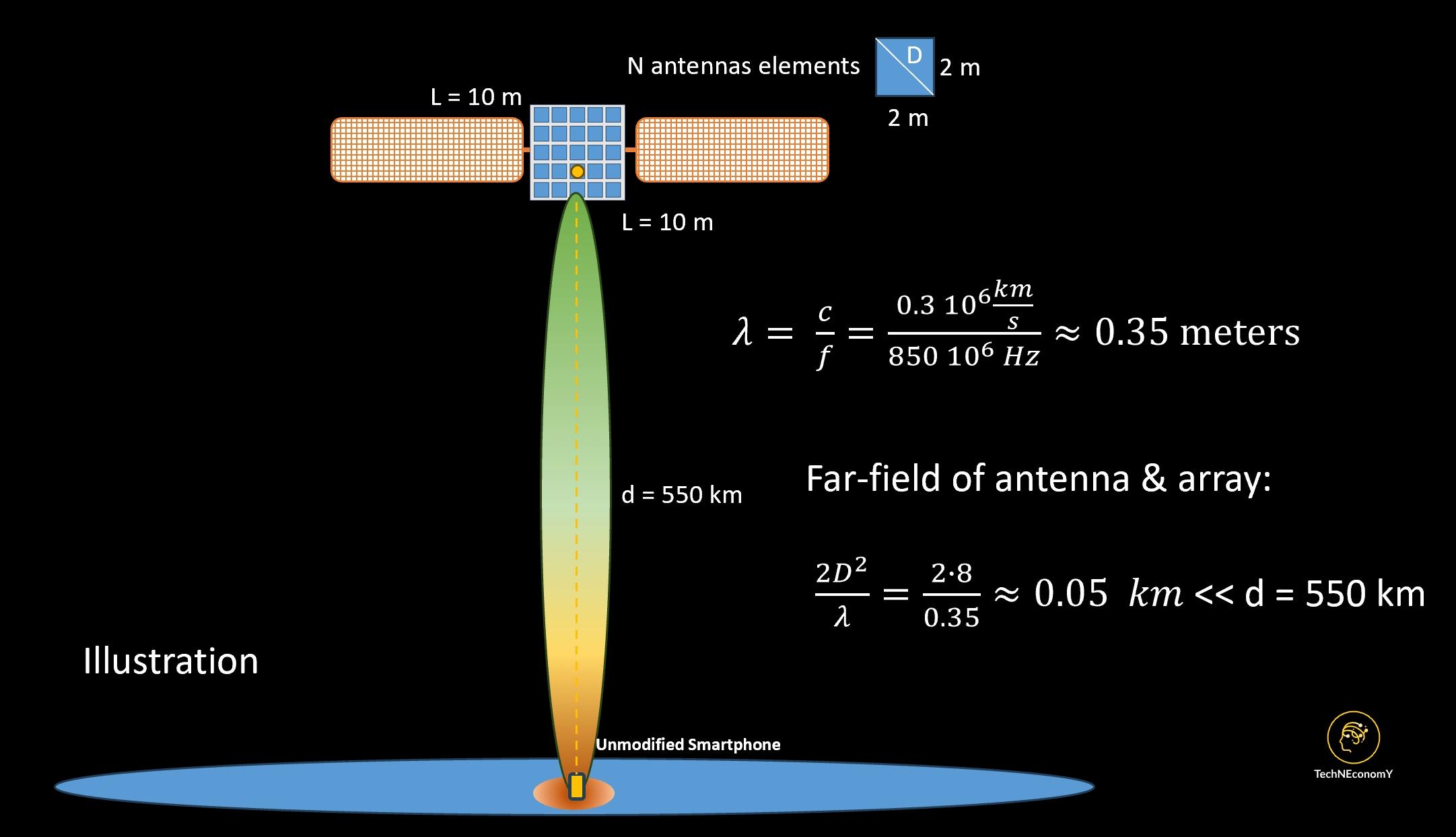

Direct-to-device LEO satellites directly connect to unmodified mobile devices such as smartphones, tablets, or other personal devices. This necessitates a design that can accommodate low-power signals and small antennas typically found on consumer devices. Therefore, these satellites often incorporate advanced beamforming capabilities through phased array antennas to focus signals precisely on specific geographic locations, enhancing signal strength and reliability for individual users. Moreover, the transceiver electronics must be highly sensitive and capable of handling simultaneous connections, each potentially requiring different levels of service quality. As the satellite provides services over remote and scarcely populated areas, at least initially, there is no need for high-capacity designs, e.g., typically requiring terrestrial cellular-like coverage areas and large frequency bandwidths. The satellites are designed to operate in frequency bands compatible with terrestrial consumer devices, necessitating coordination and compliance with various regulatory standards compared to traditional satellite services.

Implementing satellite-based SCS successfully hinges on complying with many fairly sophisticated technical requirements, such as phased array antenna design and transceiver electronics, enabling direct communication with consumer devices terrestrially. The phased array antenna, a cornerstone of this architecture, must possess advanced beamforming capabilities, allowing it to dynamically focus and steer its signal beams towards specific geographic areas or even moving targets on the Earth’s surface. This flexibility is super important for maximizing the coverage and quality of the communication link with individual devices, which might be spread across diverse and often challenging terrains. The antenna design needs to be wideband and highly efficient to handle the broad spectrum of frequencies designated for SCS operations, ensuring compatibility with the communication standards used by consumer devices (e.g., 4G LTE, 5G).

Designing phased array antennas for satellite-based direct-to-device services, envisioned by the SCS framework, requires considering various technical design parameters to ensure the system’s optimal performance and efficiency. These antennas are crucial for effective direct-to-device communication, encompassing multiple technical and practical considerations.

The SCS frequency band not only determines the operational range of the antenna but also its ability to communicate effectively with ground-based devices through the Earth’s atmosphere; in this respect, lower frequencies are better than higher frequencies. The frequency, or frequencies, significantly influences the overall design of the antenna, affecting everything from its physical dimensions to the materials used in its construction. The spacing and configuration of the antenna elements are carefully planned to prevent interference while maximizing coverage and connectivity efficiency. Typically, element spacing is kept around half the operating frequency wavelength, and the configuration involves choosing linear, planar, or circular arrays.

Beamforming capabilities are at the heart of the phased array design, allowing for the precise direction of communication beams toward targeted areas on the ground. This necessitates advanced signal processing to adjust signal phases dynamically and amplitudes, enabling the system to focus its beams, compensate for the satellite’s movement, and handle numerous connections.

The antenna’s polarization strategy is chosen to enhance signal reception and minimize interference. Dual (e.g., horizontal & vertical) or circular (e.g., right or left hand) polarization ensures compatibility with a wide range of devices and as well as more efficient spectrum use. Polarization refers to the orientation of the electromagnetic waves transmitted or received by an antenna. In satellite communications, polarization is used to differentiate between signals and increase the capacity of the communication link without requiring additional frequency bandwidth.

Physical constraints of size, weight, and form factor are also critical, dictated by the satellite’s design and launch parameters, including the launch cost. The antenna must be compact and lightweight to fit within the satellite’s structure and comply with launch weight limitations, impacting the satellite’s overall design and deployment mechanisms.

Beyond the antenna, the transceiver electronics within the satellite play an important role. These must be capable of handling high-throughput data to accommodate simultaneous connections, each demanding reliable and quality service. Sensitivity is another critical factor, as the electronics need to detect and process the relatively weak signals sent by consumer-grade devices, which possess much less power than traditional ground stations. Moreover, given the energy constraints inherent in satellite platforms, these transceiver systems must efficiently manage the power to maintain optimal operation over long durations as it directly relates to the satellite’s life span.

Operational success also depends on the satellite’s compliance with regulatory standards, particularly frequency use and signal interference. Achieving this requires a deep integration of technology and regulatory strategy, ensuring that the satellite’s operations do not disrupt existing services and align with global communication protocols.

CONCERNS.

The FCC’s Supplemental Coverage from Space (SCS) framework has been met with both anticipation and critique, reflecting diverse stakeholder interests and concerns. While the framework aims to enhance connectivity by integrating satellite and terrestrial networks, several critiques and concerns have been raised:

Interference concerns: A primary critique revolves around potential interference with existing terrestrial services. Stakeholders worry that SCS operations might disrupt the current users, including terrestrial mobile networks and other satellite services. A significant challenge is ensuring that SCS services coexist harmoniously with these incumbent services without causing harmful interference.

Certification of terrestrial mobile devices: FCC requires that terrestrial mobile devices has to be certified SCS. The expressed concerns have been multifaceted, reflecting the complexities of integrating satellite communication capabilities into standard consumer mobile devices. These concerns, as in particular highlighted in the FCC’s SCS framework, revolving around technical, regulatory, and practical aspects. As 3GPP NTN standardization are considering changes to mobile devices that would enhance the direct connectivity between device and satellite, it may at least for devices developed for NTN communication make sense to certify those.

Spectrum allocation and management: Spectrum allocation for SCS poses another concern, particularly the repurposing of spectrum bands previously dedicated to other uses. Critics argue that spectrum reallocation must be carefully managed to avoid disadvantaging existing services or limiting future innovation in those bands.

Regulatory and licensing framework: The complexity of the regulatory and licensing framework for SCS services has also been a point of contention. Critics suggest that the framework could be burdensome for new entrants or more minor players, potentially stifling innovation and competition in the satellite and telecommunications industries.

Technical and operational challenges: The technical requirements for SCS, including the need for advanced phased array antennas and the integration of satellite systems with terrestrial networks, pose significant challenges. Concerns about the feasibility and cost of developing and deploying the necessary technology at scale have been raised.

Market and economic impacts: There are concerns about the SCS framework’s economic implications, particularly its impact on existing market dynamics. Critics worry that the framework might favor certain players or technologies, potentially leading to market consolidation or barriers to entry for innovative solutions.

Environmental and space traffic management: The increased deployment of satellites for SCS services raises concerns about space debris and the sustainability of space activities. Critics emphasize the need for robust space traffic management and debris mitigation strategies to ensure the long-term viability of space operations.

Global coordination and equity: The global nature of satellite communications underscores the need for international coordination and equitable access to SCS services. Critics point out the importance of ensuring that the benefits of SCS extend to all regions, particularly those currently underserved by telecommunications infrastructure.

FURTHER READING.

- FCC-CIRC2403-03, Report and Order and further notice of proposed rulemaking, related to the following context: “Single Network Future: Supplemental Coverage from Space” (February 2024).

- A. Vanelli-Coralli, N. Chuberre, G. Masini, A. Guidotti, M. El Jaafari, “5G Non-Terrestrial Networks.”, Wiley (2024). A recommended reading for deep diving into NTN networks of satellites, typically the LEO kind, and High-Altitude Platform Systems (HAPS) such as stratospheric drones.

- Kim Kyllesbech Larsen, The Next Frontier: LEO Satellites for Internet Services. | techneconomyblog, (March 2024).

- Kim Kyllesbech Larsen, Stratospheric Drones: Revolutionizing Terrestrial Rural Broadband from the Skies? | techneconomyblog, (January 2024).

- Kim Kyllesbech Larsen, Spectrum in the USA – An overview of Today and a new Tomorrow. | techneconomyblog, (May 2023).

- Starlink, “Starlink specifications” (Starlink.com page). The following Wikipedia resource is also quite good: Starlink.

- R.K. Mailloux, “Phased Array Antenna Handbook, 3rd Edition”, Artech House, (September 2017).

- Professor Emil Björnson, “Basics of Antennas and Beamforming”, (2019). Provides a high-level understand of what beamforming is in relative simple terms.

- Professor Emil Björnson, “Physically Large Antenna Arrays: When the Near-Field Becomes Far-Reaching”, (2022). Provides a high-level understand of what phased array and their working in relative simple terms with lots of simply illustrations. I also recommend to check Prof. Björnson’s “Reconfigurable intelligent surfaces: Myths and realities” (2020).

- AST SpaceMobile website: https://ast-science.com/ Constellation Areas: Internet, Direct-to-Cell, Space-Based Cellular Broadband, Satellite-to-Cellphone. 243 LEO satellites planned. 2 launched.

- Jon Brodkin, “Google and AT&T invest in Starlink rival for satellite-to-smartphone service”, Ars Technica (January 2024). There is a very nice picture of AST’s 64 square meter large BlueWalker 3 phased array antenna (i.e., with a total supporting bandwidth of 100 MHz with a channels of 5 MHz and a theoretical spectral efficiency of 3 Mbps/MHz/channel).

- Lynk Global website: https://lynk.world/ (see also FCC Order and Authorization). It should be noted that Lynk can operate within 617 to 960 MHz (Space-to-Earth) and 663 to 915 MHz (Earth-to-Space). However, only outside the USA. Constellation Area: IoT / M2M, Satellite-to-Cellphone, Internet, Direct-to-Cell. 8 LEO satellites out of 10 planned.

- NewSpace Index: https://www.newspace.im/ I find this resource to have excellent and up-to-date information on commercial satellite constellations.

- Up-to-date rocket launch schedule and launch details can be found here: https://www.rocketlaunch.live/

ACKNOWLEDGEMENT.

I greatly acknowledge my wife, Eva Varadi, for her support, patience, and understanding during the creative process of writing this article.