Full disclosure … when I was first introduced to the concept of Network Slicing, from one of the 5G fathers that I respect immensely (Rachid, it must have been back at the end of 2014), I thought that it was one of the most useless concepts that I had heard of. I did simply not see (or get) the point of introducing this level of complexity. It did not feel right. My thoughts were that taking the slicing concept to the limit might actually not make any difference to not having it, except for a tremendous amount of orchestration and management overhead (and, of course, besides the technological fun of developing it and getting it to work).

It felt a bit (a lot, actually) as a “let’s do it because we can” thinking. With the “We can” rationale based on the maturity of cloudification and softwarization frameworks, such as cloud-native, public-cloud scale, cloud computing (e.g., edge), software-defined networks (SDN), network-function virtualization (NFV), and the-one-that-is-always-named Artificial Intelligence (AI). I believed there could be other ways to offer the same variety of service experiences without this additional (what I perceived as an unnecessary) complexity. At the time, I had reservations about its impact on network planning, operations, and network efficiency. Not at all sure, it would be a development in the right economic direction.

Since then, I have softened to the concept of Network Slicing. Not (of course) that I have much choice, as slicing is an integral part of 5G standalone (5G) implementation that will be implemented and launched over the next couple of years across our industry. Who knows, I may very likely be proven very wrong, and then I learn something.

What is a network slice? We can see a network slice as an on-user-demand logical separated network partitioning, software-defined on-top of our common physical network infrastructure (wam … what a mouthful … test me out on this one next time you see me), slicing through our network technology stack and its layers. Thinking of a virtual private network (VPN) tunnel through a transport network is a reasonably good analogy. The network slice’s logical partitioning is isolated from other traffic streams (and slices) flowing through the 5G network. Apart from the slice logical isolation, it can have many different customizations, e.g., throughput, latency, scale, Quality of Service, availability, redundancy, security, etc… The user equipment initiates the slice request from a list of pre-defined slice categories. Assuming the network is capable of supporting its requirements, the chosen slice category is then created, orchestrated, and managed through the underlying physical infrastructure that makes up the network stack. The pre-defined slice categories are designed to match what our industry believe is the most essential use-cases, e.g., (a) enhanced mobile broadband use cases (eMBB), (b) ultra-reliable low-latency communications (uRLLC) use cases, (c) massive machine-type communication (MMTC) use cases, (d) Vehicular-to-anything (V2X) use-cases, etc… While the initial (early day) applications of network slicing are expected to be fairly static and configurationally relatively simple, infrastructure suppliers (e.g., Ericsson, Huawei, Nokia, …)expect network slices to become increasingly dynamic and rich in their configuration possibilities. While slicing is typically evoked for B2B and B2B2X, there is not really a reason why consumers could not benefit from network slicing as well (e.g., gaming/VR/AR, consumer smart homes, consumer vehicular applications, etc..).

Show me the money!

Ericsson and Arthur D. Little (ADL) have recently investigated the network slicing opportunities for communications service providers (CSP). Ericsson and ADL have analyzed more than 70 external market reports on the global digitalization of industries and critically reviewed more than 400 5G / digital use cases (see references in Further Readings below). They conclude that the demand from digitalization cannot be served by CSPs without Network Slicing, e.g., “Current network resources cannot match the increasing diversity of demands over time” and “Use cases will not function” (in a conventional mobile network). Thus, according to Ericsson and ADL, the industry can not “live” without Network Slicing (I guess it is good that it comes with 5G SA then). In fact, from their study, they conclude that 30% of the 5G use cases explored would require network slicing (oh joy and good luck that it will be in our networks soon).

Ericsson and ADL find globally a network slicing business potential of 200 Billion US dollars by 2030 for CSPs. With a robust CAGR (i.e., the potential will keep growing) between 23% to 36% by 2030 (i.e., CAGR estimate for period 2025 to 2030). They find that 6 Industries segments take 90+% of the slicing potential; (1) Healthcare (23%), (2) Government (17%), (3) Transportation (15%), (4) Energy & Utilities (14%), (5) Manufacturing (12%) and (6) Media & Entertainment (11%). For the keen observer, we see that the verticals are making up for most of the slicing opportunities, with only a relatively small part being related to the consumers. It should, of course, be noted that not all CSPs are necessarily also mobile network operators (MNOs), and there are also outside the strict domain of MNOs revenue potential for non-MNO CSPs (I assume).

Let us compare this slicing opportunity to global mobile industry revenue projections from 2020 to 2030. GSMA has issued a forecast for mobile revenues until 2025, expecting a total turnover of 1,140 Billion US$ in 2025 at a CAGR (2020 – 2025) of 1.26%. Assuming this compounded annual growth rate would continue to apply, we would expect a global mobile industry revenue of 1,213 Bn US$ by 2030. Our 5G deployments will contribute in the order of 621 Bn US$ (or 51% of the total). The incremental total mobile revenue between 2020 and 2030 would be ca. 140 Bn US$ (i.e., 13% over period). If we say that roughly 20% is attributed to mobile B2B business globally, we have that by 2030 we would expect a B2B turnover of 240+ Bn US$ (an increase of ca. 30 Bn US$ over 2020). So, Ericsson & ADL’s 200 Bn US$ network slicing potential is then ca. 16% of the total 2030 global mobile industry turnover or 30+% of the 5G 2030 turnover. Of course, this assumes that somehow the slicing business potential is simply embedded in the existing mobile turnover or attributed to non-MNO CSPs (monetizing the capabilities of the MNO 5G SA slicing enablers).

Of course, the Ericsson-ADL potential could also be an actual new revenue stream untapped by today’s network infrastructures due to the lack of slicing capabilities that 5G SA will bring in the following years. If so, we can look forward to a boost of the total turnover of 16% over the GSMA-based 2030 projection. Given ca. 90% of the slicing potential is related to B2B business, it may imply that B2B mobile business would almost double due to network slicing opportunities (hmmm).

Another recent study assessed that the global 5G network slicing market will reach approximately 18 Bn US$ by 2030 with a CAGR of ca. 41% over 2020-2030.

Irrespective of the slicing turnover quantum, it is unlikely that the new capabilities of 5G SA (including network slicing and much richer granular quality of service framework) will lead to new business opportunities and enable unexplored use cases. That, in turn, may indeed lead to enhanced monetization opportunities and new revenue streams between now (2022) and 2030 for our industry.

Most Western European markets will see 5G SA being launched over the next 2 to 3 years; as 5G penetration rapidly approaches 50% penetration, I expect network slicing use cases being to be tried out with CSP/MNOs, industry partners, and governmental institutions soon after 5G SA has been launched. It should be pointed out that already for some years, slicing concepts have been trialed out in various settings. Both in 4G as well as 5G NSA networks.

Prologue to Network Slicing.

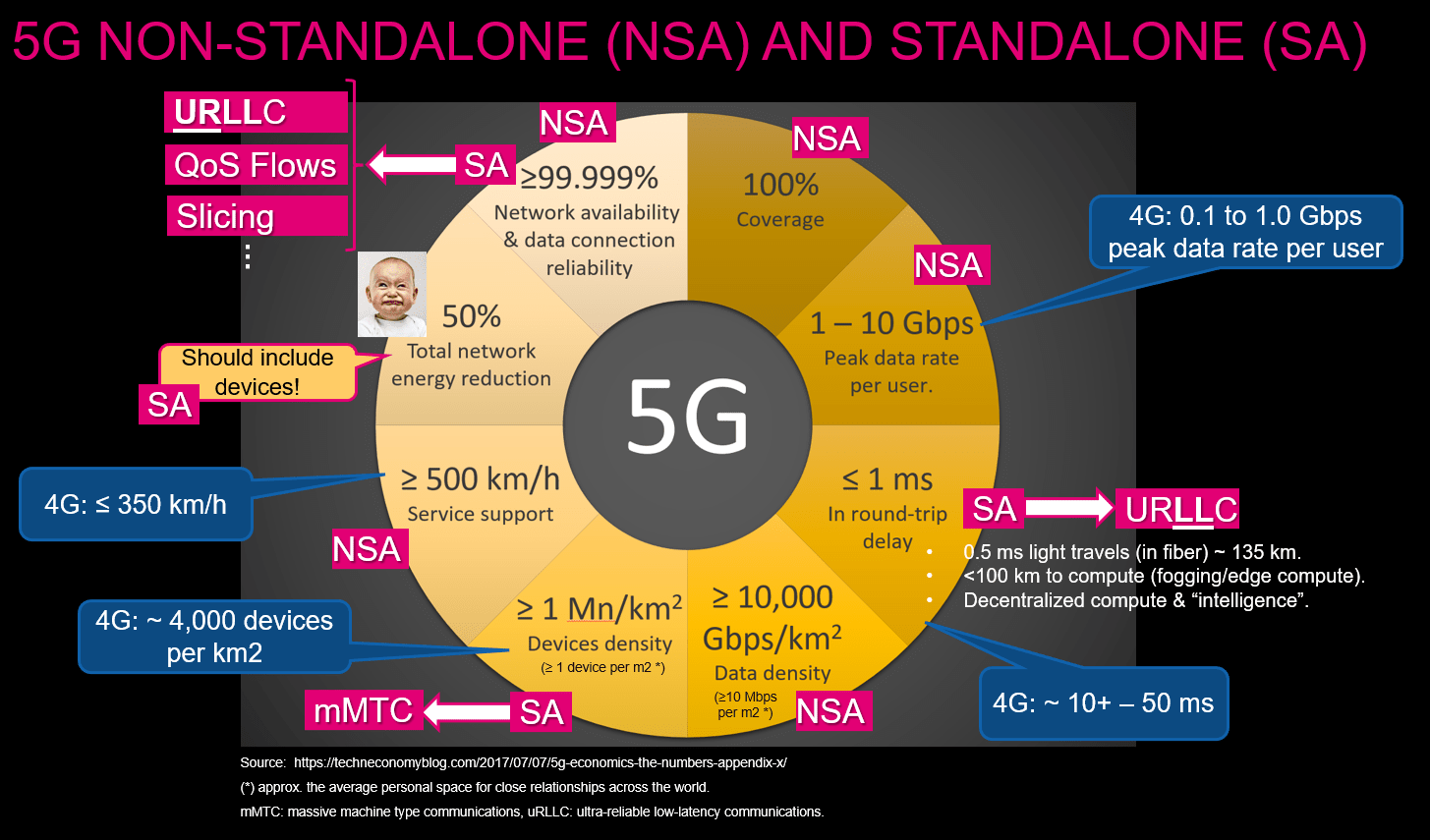

5G comes with a lot of fundamental capabilities as shown in the picture below,

5G allows for (1) enhanced mobile broadband, (2) very low latency, (3) massive increase in device density handling, i.e., massive device scale-up, (4) ultra-higher network reliability and service availability, and (5) enhanced security (not shown in the above diagram) compared to previous Gs.

The service (and thus network) requirement combinations are very high. The illustration below shows two examples of mapped-out sub-set of service (and therefore also eventually slice) requirements mapped onto the major 5G capabilities. In addition, it is quite likely that businesses would have additional requirements related to slicing performance monitoring, for example, in real-time across the network stack.

and with all the various industrial or vertical use cases (see below) one could imagine (noting that there may be many many more outside our imagination), the “fathers” of 5G became (very) concerned with how such business-critical services could be orchestrated and managed within a traditional mobile network architecture as well as across various public land mobile networks (PLMN). Much of this also comes out of the wish that 5G should “conquer” (take a slice of) next-generation industries (i.e., Industry 4.0), providing additional value above and beyond “the dumb bit pipe.” Moreover, I do believe that in parallel with the wish of becoming much more relevant to Industry 4.0 (and the next generation of verticals requirements), what also played a role in the conception of network slicing is the deeply rooted engineering concept of “control being better than trust” and that “centralized control is better than decentralized” (I lost count on this debate of centralized control vs. distributed management a long time ago).

So, yes … The 5G world is about to get a lot more complex in terms of Industrial use cases that 5G should support. And yes, our consumers will expect much higher download speeds, real-time (whatever that will mean) gaming capabilities, and “autonomous” driving …

“… it’s clear that the one shared public network cannot meet the needs of emerging and advanced mobile connectivity use cases, which have a diverse array of technical operations and security requirements.” (quote from Ericsson and Arthur D. Little study, 2021).

“The diversity of requirements will only grow more disparate between use cases — the one-size-fits-all approach to wireless connectivity will no longer suffice.” (quote from Ericsson and Arthur D. Little study, 2021).

Being a naturalist (yes, I like “naked” networks), it does seem somewhat odd (to me) to say that next generation (e.g., 5G) networks cannot support all the industrious use cases that we may throw at it in its native form. Particular after having invested billions in such networks. By partitioning a network up in limiting (logically isolated), slice instances can all be supported (allegedly). I am still in the thinking phase on that one (but I don’t think the math adds up).

Now, whether one agrees (entirely) with the economic sentiment expressed by Ericsson and ADL or not. We need a richer granular way of orchestrating and managing all those diverse use-cases we expect our 5G network to support.

Network Slicing.

So, we have (or will get) network slicing with our 5G SA Core deployment. As a reminder, when we talk about a network slice, we mean;

“An on-user-demand logical separated network partitioning, software-defined, on-top of a common physical network infrastructure.”

So, the customer requested the network slice, typically via a predefined menu of slicing categories that may also have been pre-validated by the relevant network. Requested slices can also be Customized, by the requester, within the underlying 5G infrastructure capabilities and functionalities. If the network can provide the requested slicing requirements, the slice is (in theory) granted. The core network then orchestrates a logically separated network partitioning throughout the relevant infrastructure resources to comply with the requested requirements (e.g., speed, latency, device scale, coverage, security, etc…). The requested partitioning (i.e., the slice) is isolated from other slices to enable (at least on a logical level) independence of other live slices. Slice Isolation is an essential concept to network slicing. Slice Elasticity ensures that resources can be scaled up and down to ensure individual slice efficiency and an overall efficient operation of all operating slices. It is possible to have a single individual network slice or partition a slice into sub-slices with their individual requirements (that does not breach the overarching slice requirements). GSMA has issued roaming and inter-PLMN guidelines to ensure 5G network slicing inter-operability when a customer’s application finds itself outside its home -PLMN.

Today, and thanks to GSMA and ITU, there are some standard network slice services pre-defined, such as (a) eMBB – Enhanced Mobile Broadband, (b) mMTC – Massive machine-type communications, (c) URLLC – Ultra-reliable low-latency communications, (d) V2X – Vehicular-to-anything communications. These identified standard network slices are called Slice Service Types (SST). SSTs are not only limited to above mentioned 4 pre-defined slice service types. The SSTs are matched to what is called a Generic Slice Template (GST) that currently, we have 37 slicing attributes, allowing for quite a big span of combinations of requirements to be specified and validated against network capabilities and functionalities (maybe there is room for some AI/ML guidance here).

The user-requested network slice that has been set up end-2-end across the network stack, between the 5G Core and the user equipment, is called the network slice instance. The whole slice setup procedure is very well described in Chapter 12 of “5G NR and enhancements, from R15 to R16. The below illustration provides a high-level illustration of various network slices,

The 5G control function Access and Mobility management Function (AMF) is the focal point for the network slicing instances. This particular architectural choice does allow for other slicing control possibilities with a higher or lower degree of core network functionality sharing between slice instances. Again the technical details are explained well in some of the reading resources provided below. The takeaway from the above illustration is that the slice instance specifications are defined for each layer and respective physical infrastructure (e.g., routers, switches, gateways, transport device in general, etc…) of the network stack (e.g., Telco Core Cloud, Backbone, Edge Cloud, Fronthaul, New Radio, and its respective air-interface). Each telco stack layer that is part of a given network slice instance is supposed to adhere strictly to the slice requirements, enabling an End-2-End, from Core to New Radio through to the user equipment, slice of a given quality (e.g., speed, latency, jitter, security, availability, etc..).

And it may be good to keep in mind that although complex industrial use cases get a lot of attention, voice and mobile broadband could easily be set up with their own slice instances and respective quality-of-services.

Network slicing examples.

All the technical network slicing “stuff” is pretty much-taken care of by standardization and provided by the 5G infrastructure solution providers (e.g., Mavenir, Huawei, Ericsson, Nokia, etc..). Figuring the technical details of how these works require an engineering or technical background and a lot of reading.

As I see it, the challenge will be in figuring out, given a use-case, the slicing requirements and whether a single slice instance suffice or multiple are required to provide the appropriate operations and fulfillment. This, I expect, will be a challenge for both the mobile network operator as well as the business partner with the use case. This assumes that the economics will come out right for more complex (e.g., dynamic) and granular slice-instance use cases. For the operator as well as for businesses and public institutions.

The illustration below provides examples of a few (out of the 37) slicing attributes for different use cases, (a) Factories with time-critical, non-time-critical, and connected goods sub-use cases (e.g., sub-slice instances, QoS differentiated), (b) Automotive with autonomous, assisted and shared view sub-use cases, (c) Health use cases, and (d) Energy use cases.

One case that I have been studying is Networked Robotics use cases for the industrial segment. Think here about ad-hoc robotic swarms (for agricultural or security use cases) or industrial production or logistics sorting lines; below are some reflections around that.

End thoughts.

With the emergence of the 5G Core, we will also get the possibility to apply Network slicing to many diverse use cases. That there are interesting business opportunities with network slicing, I think, is clear. Whether it will add 16% to the global mobile topline by 2030, I don’t know and maybe also somewhat skeptical about (but hey, if it does … fantastic).

Today, the type of business opportunities that network slicing brings in the vertical segments is not a very big part of a mobile operator’s core competence. Mobile operators with 5G network slicing capabilities ultimately will need to build up such competence or (and!) team up with companies that have it.

That is, if the future use cases of network slicing, as envisioned by many suppliers, ultimately will get off the ground economically as well as operationally. I remain concerned that network slicing will not make operators’ operations less complex and thus will add cost (and possible failures) to their balance sheets. The “funny” thing (IMO) is that when our 5G networks are relatively unloaded, we would not have a problem delivering the use cases (obviously). Once our 5G networks are loaded, network slicing may not be the right remedy to manage traffic pressure situations or would make the quality we are providing to consumers progressively worse (and I am not sure that business and value-wise, this is a great thing to do). Of course, 6G may solve all those concerns 😉

Acknowledgement.

I greatly acknowledge my wife, Eva Varadi, for her support, patience, and understanding during the creative process of writing this Blog. Also, many of my Deutsche Telekom AG and Industry colleagues, in general, have in countless ways contributed to my thinking and ideas leading to this little Blog. Thank you!

Further readings.

Kim Kyllesbech Larsen, “5G Standalone – European Demand & Expectations (Part I).”, LinkedIn article, (December 2021).

Kim Kyllesbech Larsen, “5G Economics – The Numbers (Appendix X).”, Techneconomyblog.com, (July 2017).

Kim Kyllesbech Larsen, “5G Economics – The Tactile Internet (Chapter 2)”, Techneconomyblog.com, (January 2017).

Henrik Bailier, Jan Lemark, Angelo Centonza, and Thomas Aasberg, “Applied network slicing scenarios in 5G”, Ericsson Technology Review, (February 2021).

Ericsson and Arthur D. Little, “Network slicing: A go-to-market guide to capture the high revenue potential”, Ericsson.com, (2021). The study concludes that network slicing is a 200 Bn. US$ opportunity for CSPs by 2030. It is 1 out of 4 reports on network slicing. See also “Network slicing: Top 10 use cases to target”, “The essential building blocks of E2E network slicing” and “The network slicing transformation journey“.

S. O’Dea, “Global mobile industry revenue from 2016 to 2025″, (March, 2021).

S. M. Ahsan Kazmi, Latif U.Khan, Nguyen H. Tran, and Choong Seon Hong, “Network Slicing for 5G and Beyond Networks”, Springer International Publishing, (2019).

Jia Shen, Zhongda Du, & Zhi Zhang, “5G NR and enhancements, from R15 to R16”, Elsevier Science, (2021). Provides a really good overview of what to expect from 5G standalone. Chapter 12 provides a good explanation of (and in detail account for) how 5G Network Slicing works in detail. Definitely one of my favorite books on 5G, it is not “just” an ANRA.

GSMA Association, “An Introduction to Network Slicing”, (2017). A very good introduction to Network slicing.

ITU-T, “Network slice orchestration and management for providing network services to 3rd party in the IMT-2020 network”, Recommendation ITU-T Y.3153 (2019). Describing high-level customer slice request for instantiation, changes and ultimately the termination.

Claudia Campolo, Antonella Molinaro, Antonio Lera, and Francesco Menichella, “5G Network Slicing for Vehicle-to-Everything Services”, IEEE Wireless Communications 24, (December 2017). Great account of how network slicing should work for V2X services.

GSMA, “Securing the 5G Era” (2021). A good overview of security principles in 5G and how previous vulnerabilities in previous cellular generations are being addressed in 5G. This includes some explanation on why slicing further enhances security.