As I am preparing for my keynote speech for the Annual Dinner event of the Telecom Society Netherlands (TSOC) end of January 2020, I thought the best way was to write down some of my thoughts on the key question “Is the ‘Uber’ moment for the telecom sector coming?”. In the end it turned out to be a lot more than some of my thoughts … apologies for that. Though it might still be worth reading, as many of those considerations in this piece will be hitting a telcos near you soon (if it hasn’t already).

Knowing Uber Technologies Inc’s (Uber) business model well (and knowing at least the Danish taxi industry fairly well as my family has a 70+ years old Taxi company, Radio-Taxi Nykoebing Sjaelland Denmark, started by my granddad in 1949), it instinctively appear to be an odd question … and begs the question “why would the telecom sector want an Uber moment?” … Obviously, we would prefer not to be massively loss making (as is the Uber moment at this and past moments, e.g., several billions of US$ loss over the last couple of years) and also not the regulatory & political headaches (although we have our own). Not to mention some of the negative reputation issues around “their” customer experience (quiet different from telco topics and thank you for that). Also not forgetting that Uber has access to only a fraction of the value chain in the markets the operate … Althans of course Uber is also ‘infinitely’ lighter in terms of assets than a classical Telco … Its also a bit easier to replicate an Uber (or platform businesses in general) than an asset-heavy Telco (as it requires a “bit” less cash to get started;-). But but … of course the question is more related to the type of business model Uber represent rather than the taxi / ride hailing business model itself. Thinking of Uber makes such a question more practical and tangible …

And not to forget … The super cool technology aspects of being a platform business such as Uber … maybe Telco-land can and should learn from platform businesses? … Lets roll!

uber Uber

Uber main business (ca. 81%) is facilitating peer-2-peer ride sharing and ride hailing services via their mobile application and its websites. Uber tabs into the sharing economy. Making use of under-utilized private cars and their owners (producers) willingness to give up hours of their time to drive others (consumers) around in their private vehicle. Uber had 95 million active users (consumers) in 2018 and is expected to reach 110 million in 2019 (22% CAGR between 2016 & 2019). Uber has around 3+ million drivers (producers) spread out over 85+ countries and 900+ cities around the world (although 1/3 is in the USA). In the third quarter of 2019, Uber did 1.77 billion trips. That is roughly 200 trips per Uber driver per month of which the median income is 155 US$ per month (1.27 US$ per trip) before gasoline and insurances. In December 2017, the median monthly salary for Americans was $3,714.

In addition Uber also provides food delivery services (i.e., Uber Eats, ca. 11%), Uber Freight services (ca. 7%) and what they call Other Bets (ca. 1%). The first 9 month of 2019, Uber spend more than 40% of the turnover on R&D. Uber has an average revenue per trip (ARPT) of ca. 2 US$ (out of 9.5 US$ per trip based on gross bookings). Not a lot of ARPT growth the last 9 quarters. Although active users (+30% YoY), trips (+31% YoY), Gross Bookings (+32%) and Adjusted Net Revenue (+35%) all shows double digit growth.

Uber allegedly takes a 25% fee of each fare (note: if you compare gross bookings, the total revenue generated by their services, to net revenue which Uber receives the average is around 20%).

Uber’s market cap, roughly 10 years after being founded, after its IPO was 76 Bn US$ (@ May 10th, 2019) only exceeded by Facebook (104.2 Bn @ IPO) and Alibaba Group (167.6 Bn US$ @ IPO). 7 month after Uber’s market cap is ca. 51 Bn US$ (-33% down on IPO). The leading European telco Deutsche Telekom AG (25 years old, 1995) in comparison has a market capitalization around 70 Bn US$ and is very far from loss making. Deutsche Telekom is one of the world’s leading integrated telecommunications companies, with some 170+ million mobile customers, 28 million fixed-network lines, and 20 million broadband lines.

Peal the Onion

“Telcos are pipe businesses, Ubers are platform businesses”

In other words, Telco’s are adhering to a classical business model with fairly linear causal value chain (see Michael Porter’s classic from 1985). It’s the type of input/output businesses that has been around since the dawn of the industrial revolution. Such a business model can (and should) have a very high degree of end-2-end customer experience control.

Ubers (e.g., Uber, Airbnb, Booking.com, ebay, Tinder, Minecraft, …) are non-linear business models that benefit from direct and indirect network effects allowing for exponential growth dynamics. Such businesses are often piggybacking on under-utilized or un-used assets owned by individuals (e.g., homes & rooms, cars, people time, etc…). Moreover, these businesses facilitate networked connectivity between consumers and producers via a digital platform. As such, platform businesses rarely have complete end-2-end customer experience control but would focus on the quality and experience of networked connectivity. While platform business have little control over their customers (i.e., consumers and producers) experiences or overall customer journey they may have indirectly via near real-time customer satisfaction feedback (although this is after the fact).

Clearly the internet has enabled many new ways of doing business. In particular it allows for digital businesses (infrastructure lite) to create value by facilitating networked-scaled business models where demand (i.e., customers demand XYZ) and supply (i.e., businesses supplying XYZ).

Think of Airbnb‘s internet-based platform that connects (or networks) consumers (guests), who are looking for temporary accommodation (e.g., hotel room), with producers (hosts, private or corporate) of temporary accommodations to each other. Airbnb thus allow for value creation by tying into the sharing economy of private citizens. Under-utilized private property is being monetized, benefiting hosts (producers), guests (consumers) and the platform business (by charging a transactional fee). Airbnb charges hosts a 3% fee that mainly covers the payment processing cost. Moreover, Airbnb’s typical guest fee is under 13% of the booking cost. “Airbnb is a platform business built upon software and other peoples under-utilized homes & rooms”. While Airbnb facilitated private (temporary) accommodations to consumers, today there are other online platform businesses (e.g., Booking.com, Experia.com, agoda.com, … ) that facilitates connections between hotels and consumers.

Think of Uber‘s online ride hailing platform connects travelers (consumer) with drivers (producers, private or corporate) as an alternative to normal cab / taxi services. Uber benefits from the under-utilization of most private cars, the private owners willingness to spend spare time and desire to monetize this under-utilization by becoming a private cab driver. Again the platform business exploring the sharing economy. Uber charges their drivers 25% of the faring fee. “Uber is a platform business built upon software and other peoples under-utilized cars and spare time”. The word platform was used 747 times in Uber’s IPO document. After Uber launched its digital online ride hailing platform, many national and regional taxi applications have likewise been launched. Facilitating an easier and more convenient way of hauling a taxi, piggybacking on the penetration of smartphones in any given market. In those models official taxi businesses and licensed taxi drivers collaborate around an classical industry digital platform facilitating and managing dispatches on consumer demand.

“A platform business relies on the sharing economy, monetizing networking (i.e., connecting) consumers and producers by taking a transaction fee on the value of involved transaction flow.”

E.g., consumer pays producer, or consumer get service for free and producer pays the platform business. It is a highly scaleble business model with exponential potential for growth assuming consumers and producers alike adapt your platform. The platform business model tends to be (physical) infrastructure and asset lite and software heavy. It typically (in start-up phase at least) relies on commercially available cloud offering (e.g., Lyft relies on AWS, Uber on AWS & Google) or if the platform business is massively scaled (e.g., Facebook), the choice may be to own data center infrastructure to have better platform control over operations. Typically you will see that successful Platform businesses at scale implements hybrid cloud model levering commercially available cloud solutions and own data centers. Platform businesses tend to be heavily automated (which is relative easy in a modern cloud environment) and rely very significantly on monetizing their data with underlying state-of-the-art real-time big data systems and of course intelligent algorithmic (i.e., machine learning based) business support systems.

Consider this

A platform-business’s technology stack, residing in a cloud, will typically run on a virtual machine or within a so-called container engine. The stack really resides on the upper protocol layers and is transparent to lower level protocols (e..g, physical, link, network, transport, …). In general the platform stack can be understood to function on the 3 platform layers presented in the chart to the left; (top-platform-layer) Networked Marketplace that connects producers and consumers with each other. This layer describes how a platform business customers connect (e.g., mobile app on smartphone), (middle-platform-layer) Enabling Layer in which microservices, software tools, business logic, rules and so forth will reside, (bottom-platform-layer) the Big Data Layer or Data Layer with data-driven decision making are occurring often supported by advanced real-time machine learning applications. The remaining technology stuff (e.g., physical infrastructure, servers, storage, LAN/WAN, switching, fixed and mobile telco networking, etc..) is typically taken care of by cloud or data center providers and telco providers. Which is explains why platform businesses tends to be infrastructure or asset lite (and software heavy) compared to telco and data-center providers.

“Many classical linear businesses are increasingly copying the platform businesses digital strategies (achieving an improved operational excellence) without given up on their fundamental value-chain control. Thus allowing to continue to provide consumers a known and often improved customer experience compared to a pure platform business.”

So what about the Telco model?

Well, the Telco business model is adhering to a linear value chain and business logic. And unless you are thinking of a service telco provider or virtual telco operator, Telcos are incredible infrastructure and asset heavy with massive capital investments required to provide competitive services to their customers. Apart from the required capital intensive underlying telco technology infrastructure, the telco business model requires; (1) public licenses to operate (often auctioned, or purchased and rarely “free”), (2) requires (public) telephony numbers, (3) spectrum frequencies (i.e.,for mobile operation) and so forth …

Furthermore, overall customer experience and end-2-end customer journey is very important to Telcos (as it is to most linear businesses and most would and should subscribe to being very passionate about it). In comparison to Platform Businesses, it would not be an understatement (at this moment in time at least) to say that most Telco businesses are lagging on cloudification/softwarisation, intelligent automation (whether domain-based or End-2-End) and advanced algorithmic (i.e., machine learning enabled) decision making as it relates to overarching business decisions as well as customer-related micro-decisions. However, from an economical perspective we are not talking about more than 10% – 20% of a Telco’s asset base (or capital expenses).

Mobile telco operators tend to be fairly advanced in their approaches to customer experience management, although mainly reactive rather than pro-active (due to lower intelligent algorithmic maturity again in comparison to most platform businesses). In general, fixed telco businesses are relative immature in their approaches to customer experience management (compared to mobile operators) possibly due lack of historical competitive pressure (“why care when consumers have not other choice” mindset). Alas this too is changing as more competition in fixed telco-land emerges.

“Telcos have some technology catching up to do in comparison & where relevant with platform businesses. However, that catching up does not force them to change the fundamentals of their business model (unless it make sense of course).”

Characteristic of a Platform Business

- Often relies on the sharing economy (i.e., monetizing under-utilized resources).

- It’s (exponential) growth relies on successful networking of consumers & producers (i.e., piggybacking on network effects).

- Software-centric: platform business is software and focus / relies on the digital domain & channels.

- Mobile-centric: mobile apps for consumers & producers.

- Cloud-centric: platform-solution built on Public or Hybrid cloud models.

- Cloud-native maturity level (i.e., the highest cloud maturity level).

- Heavily end-2-end automated across cloud-native platform, processes & decision making.

- Highly sophisticated data-driven decision making.

- Infrastructure / asset lite (at scale may involve own data center assets).

- Business driven & optimized by state-of-art big data real-time solutions supported by a very high level of data science & engineering maturity.

- Little or no end-2-end customer experience control (i.e., in the sense of complete customer journey).

- Very strong focus on connection experience including payment process.

- Revenue source may be in form of transactional fee imposed on the value involved in networking producers and consumers (e.g., payment transaction, cost-per-click, impressions, etc..).

In my opinion it is not a given that a platform business always have to disrupt an existing market (or classical business model). However, a successful platform business often will be transformative, resulting in classical business attempting to copy aspects of the platform business model (e..g, digitalization, automation, cloud transformation, etc..). It is too early in most platform businesses life-cycle to conclude whether, where they disrupt, it is a temporary disruption (until the disrupted have transformed) or a permanently destruction of an existing classical market model (i.e., leaving little or no time for transformation).

So with the above in mind (and I am sure for many other defining factors), it is hard to see a classical telco transforming itself into a carbon copy of a platform business and maybe more importantly why this would make a lot of sense to do in the first instance. But but … it is also clear that Telco-land should proudly copy what make sense (e.g., particular around tech and level of digitization).

Teaser thought Though if you think in terms of sharing economical principles, the freedom that an eSIM (or software-based SIM equivalents) provides with 5 or more network profiles may bring to a platform business going beyond traditional MVNOs or Service Providers … well well … you think! (hint: you may still need an agreement with the classical telco though … if you are not in the club already;-). Maybe a platform model could also tab into under-utilized consumer resources that the consumer has already paid for? or what about a transactional model on Facebook (or other social media) where the consumer actual monetizes (and controls) personal information directly with third party advertisers? (actually in this model the social media company could also share part of its existing spoil earned on their consumer product, i.e., the consumer) etc…

However, it does not mean that telcos cannot (and should not) learn from some of the most successful platform business around. There certainly is enough classical beliefs in the industry that may be ripe for a bit of disruption … so untelconizing (or as my T-Mobile US friends like to call it uncarrier) ourselves may not be such a bad idea.

Telco-land

“There is more to telco technologies than its core network and backend platforms.”

Having a great (=successful) e-commerce business platform with cloud-native maturity level including automation that most telcos can only dream of, and mouth watering real-time big data platforms with the smartest data scientist and data engineers in the world … does not make for an easy straightforward transformation to a national (or world for that matter) leading (or non-leading) telco business in the classical sense of owning the value chain end-to-end.

Japan’s Rakuten is one platform business that has the ambition and expressed intention to move from being traditional platform-based business (ala Amazon.com) to become a mobile operator leveraging all the benefits and know-how of their existing platform technologies. Extending those principles, such as softwarization, cloudification and cloud-native automation principles, all the way out to the edge of the mobile antenna.

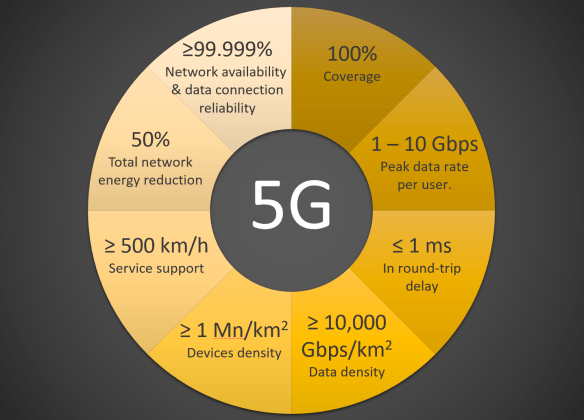

Many of us in telco-land thought that starting out with a classical telco, with mobile and maybe fixed assets as well, would make for an easy inclusion of platform-like technologies (as describe above), have had to revise our thinking somewhat. Certainly time-lines have been revised a couple of times, as have the assumed pre-conditions or context for such a transformation. Even economical and operational benefits that seems compelling, at least from a Greenfield perspective, turns out to be a lot more muddy when considering the legacy spaghetti we have in telcos with years and years in bag. And for the ones who keep saying that 5G will change all that … no I really doubt that it will any time soon.

While above platform-like telco topology looks so much simpler than the incumbent one … we should not forget it is what lays underneath the surface that matters. And what matters is software. Lots of software. The danger will always be present that we are ending up replacing hardware & legacy spaghetti complexity with software spaghetti complexity. Resulting unintended consequences in terms of longer-term operational stability (e.g,, when you go beyond being a greenfield business).

“Software have made a lot in the physical world redundant but it may also have leapfrogged the underlying operational complexity to an extend that may pose an existential threat down the line.”

While many platform businesses have perfected cloud-native e-commerce stacks reaching all the way out to the end-consumers mobile apps, residing on the smartphone’s OS, they do operate on the higher level of whatever relevant telco protocol stack. Platform businesses today relies on classical telcos to provide a robust connection data pipe to their end-users at high availability and stability.

What’s coming for us in Telco-land?

“Software will eat more and more of telco-land’s hardware as well as the world.”

(side note: for the ones who want to say that artificial intelligence (AI) will be eating the software, do remember that AI is software too and imo we talk then about autosarcophagy … no further comment;-).

Telcos, of the kinds with a past, will increasingly implement software solutions replacing legacy hardware functionality. Such software will be residing in a cloud environment either in form of public and/or private cloud models. We will be replacing legacy hardware-centric telco components or boxes with a software copy, residing on a boring but highly standardized hardware platform (i.e., a common off the shelf server). Yes … I talk about software definable networks (SDN) and network functional virtualization (NFV) features and functionalities (though I suspect SDN/NFV will be renamed to something else as we have talked about this for too many years for it to keep being exciting;-). The ultimate dream (or nightmare pending on taste) is to have all telco functions defined in software and operating on a very low number of standardized servers (let’s call it the pizza-box model). This is very close to the innovative and quiet frankly disruptive ideas of for example Drivenets in Israel (definitely worth a study if you haven’t already peeked at some of their solutions). We are of course seeing quiet some progress in developing software equivalents to telco core (i.e., Telco Cloud in above picture) functionalities, e.g., evolved packet core (EPC) functions, policy and charging rules function (PCRF), …. These solutions are available from the usual supplier suspects (e.g., Cisco, Ericsson, Huawei, and Nokia) as well as from (relative) new bets, such as for example Affirmed Networks and Mavenir (side note: if you are not the usual supplier suspect and have developed cloud-based telco functionalities drop me a note … particular if such work in a public or hybrid cloud model with for example Azure or AWS).

We will have software eating its way out to the edge of our telco networks. That is assuming it proves to make economical and operational sense (and maybe even anyway;-). As computing requirements, driven by softwarization of telco-land, goes “through the roof” across all network layers, edge computing centers will be deployed (or classical 2G BSC or 3G RNC sites will be re-purposed for the “lucky” operators with a more dis-aggregated network typologies).

Telcos (should) have very strong desires for platform-like automation as we know it from platform businesses cloud-native implementations. For a telco though, the question is whether they can achieve cloud-native automation principles throughout all their network layers and thus possibly allow for end-2-end (E2E) automation principles as known in a cloud-native world (which scope wise is more limited than the full telco stack). This assumes that an E2E automation goal makes economical and operational sense compared to domain-oriented automation (with domains not per see matching one to one the traditional telco network layers). While it is tempting to get all enthusiastic & winded-up about the role of artificial intelligence (AI) in telco (or any other) automation framework, it always make sense to take an ice cold shower and read up on non-AI based automation schemes as we have them in a cloud-native cloud environment before jumping into the rabbit hole. I also think that we should be very careful architecturally to spread intelligent agents all over our telco architecture and telco stack. AI will have an important mission in pro-active customer experience solutions and anomaly detection. The devil may be in how we close the loop of an intelligent agent’s output and a input to our automation framework.

To summarize what’s coming for the Telco sector;

- Increased softwarization (or virtualization) moving from traditional platform layers out towards the edge.

- Increased leveraging of cloud models (e.g., private, public, hybrid) following the path of softwarization.

- Strive towards cloud-native operations including the obvious benefits from (non-AI based) automation that the cloud-native framework brings.

- We will see a lot of focus on developing automation principles across the telco stack to the extend such will be different from cloud-native principles (note: expect there will be some at least for non-Greenfield implementations but also in general as the telco stack is not idem ditto a traditional platform stack). This may be hampered by lack of architectural standardization alignment across our industry. There is a risk that we will push for AI-based automation without exploring fully what non-AI based schemes may bring.

- Inevitable the industry will spend much more efforts on developing cognitive-based pro-active customer experience solutions as well as expanding anomaly detection across the full telco stack. This will help in dealing with design complexities although might also be hampered by mis-alignment on standardization. Not to mention that AI should never become an excuse to not simplify designs and architectures.

- Plus anything clever that I have not thought about or forgot to mention 🙂

So yes … softwarization, cloudification and aggressive (non-AI based) automation, known from platform-centric businesses, will be coming (in fact has arrived to an extend) for Telcos … over time and earlier for the few new brave Telco Greenfields …

Artificial intelligence based solutions will have a mission in pro-active customer experience (e.g., cellwize, uhana, …), zero-touch predictive maintenance, self-restoration & healing, and for advanced anomaly detection solutions (e.g., see Anodot as a leading example here). All are critical requirements in the new (and obviously in the old as well) telco world is being eaten by software. Self-learning “conscious” (defined in a relative narrow technical sense) anomaly detection solutions across the telco stack is in my opinion a must to deal with today’s and the future’s highly complex software architectures and systems.

I am also speculating whether intelligent agents (e.g., microagents reacting to an events) may make the telco layers less reliant on top-down control and orchestration (… I am also getting goosebumps by that idea … so maybe this is not good … hmmm … or I am cold … but then again orchestration is for non-trusting control “freaks”). Such a reactive microagent (or microservice) could take away the typical challenges with stack orchestration (e.g., blocking, waiting, …), decentralize control across the telco stack.

And no … we will not become Ubers … although there might be Ubers that will try to become us … The future will show …

Acknowledgement.

I also greatly acknowledge my wife Eva Varadi for her support, patience and understanding during the creative process of writing this Blog. Also many of my Deutsche Telekom AG, T-Mobile NL & Industry colleagues in general have in countless of ways contributed to my thinking and ideas leading to this little Blog. Thank you!

Further reading

Mike Isaac, “Super Pumped – The Battle for Uber”, 2019, W.W. Norton & Company. A good read and what starts to look like a rule of a Silicon Valley startup behavior (the very worst and of course some of the best). Irrespective of the impression this book leaves with me, I am also deeply impressed (maybe even more after reading the book;-) what Uber’s engineers have been pulling off over the last couple of years.

Muchneeded.com, “Uber by the Numbers: Users & Drivers Statistics, Demographics, and Fun Facts”, 2018. The age of the Uber statistics presented varies a lot. It’s a nice overall summary but for most recent stats please check against financial reports or directly from Uber’s own website.

Graham Rapier, “Uber lost $5.2 billion in 3 months. Here’s where all that money went”, 2019, Business Insider. As often is the case with web articles, it is worth actually reading the article. Out of the $5.2 billion, $3.9 Billion was due to stock-based compensation. Still a loss of $1.3 billion is nevertheless impressive as well. In 2018 the loss was $1.8 billion and $4.5 billion in 2017.

Chris Anderson, “Free – The Future of a Radical Price”, (2009), Hyperion eBook. This is one of the coolest books I have read on the topic of freemium, sharing economy and platform-based business models. A real revelations and indeed a confirmation that if you get something for free, you are likely not a customer but a product. A must read to understand the work around us. In this setting it is also worth reading “What is a Free Customer Worth?” by Sunil Gupta & Carl F. Mela (HBR, 2008).

Sangeet Paul Choudary, “Platform Scale”, (2015), Platform Thinking Labs Pte. Ltd. A must read for anyone thinking of developing a platform based business. Contains very good detailed end-2-end platform design recommendations. If you are interested in knowing the most important aspects of Platform business models and don’t have time for more academic deep dive, this is most likely the best book to read.

Laure Claire Reillier & Benout Reillier, “Platform Strategy”, (2017), Routledge Taylor & Francis Group. Very systematic treatment of platform economics and all strategic aspects of a platform business. It contains a fairly comprehensive overview of academic works related to platform business models and economics (that is if you want to go deeper than for example Choudary’s excellent “Platform Scale” above).

European Commission Report on “Study on passenger transport by taxi, hire car with driver and ridesharing in the EU”, (2016), European Commission.

Michal Gromek, “Business Models 2.0 – Freemium & Platform based business models“, (2017), Slideshare.net.

Greg Satell, “Don’t Believe Everything You Hear About Platform Businesses”, (2018), Inc.. A good critique of the hype around platform business models.

Jean-Charles Rochet & Jean Tirole, “Platform Competition in Two-sided Markets” (2003), Journal of the European Economic Association, 1, 990. Rochet & Tirole formalizes the economics of two-sided markets. The math is fairly benign but requires a mathematical background. Beside the math their paper contains some good descriptions of platform economics.

Eitan Muller, “Delimiting disruption: Why Uber is disruptive, but Airbnb is not”, (2019), International Journal of Research in Marketing. Great account (backed up with data) for the disruptive potential of platform business models going beyond (and rightly so) Clayton Christensen Disruptive Theory.

Todd W. Schneider, “Taxi and Ridehailing Usage in New York City”, a cool site that provides historical and up-to-date taxi and ride hailing usage data for New York and Chicago. This gives very interesting insights into the competitive dynamics of Uber / Ride hailing platform businesses vs the classical taxi business. It also shows that while ride hailing businesses have disrupted the taxi business in totality, being a driver for a ride hailing platform is not that great either (and as Uber continues to operate at impressive losses maybe also not for Uber either at least in their current structure).

Uber Engineering is in general a great resource for platform / stack architecture, system design, machine learning, big data & forecasting solutions for a business model relying on real-time transactions. While I personally find the Uber architecture or system design too complex it is nevertheless an impressive solution that Uber has developed. There are many noteworthy blog posts to be found on the Uber Engineering site. Here is a couple of foundational ones (both from 2016 so please be aware that lots may have changed since then) “The Uber Engineering Tech Stack, Part I: The Foundation” (Lucie Lozinski, 2016) and “The Uber Engineering Tech Stack, Part II: The Edge and Beyond” (Lucie Lozinski, 2016) . I also found “Uber’s Big Data Platform: 100+ Petabytes with Minute Latency” post (by Reza Shiftehfar, 2018) very interesting in describing the historical development and considerations Uber went through in their big data platform as their business grew and scale became a challenge in their designs. This is really a learning resource.

Wireless One, “Rakuten: Japan’s new #4 is going all cloud”, 2019. Having had the privilege to visit Rakuten in Japan and listen to their chief-visionary Tareq Amin (CTO) they clearly start from being a platform-centric business (i.e., Asia’s Amazon.com) with the ambition to become a new breed of telco levering their platform technologies (and platform business model thinking) all the way out to the edge of the mobile base station antenna. While I love that Tareq Amin actually has gone and taken his vision from powerpoint to reality, I also think that Rakuten benefits (particular many of the advertised economical benefits) from being more a Greenfield telco than an established telco with a long history and legacy. In this respect it is humbling that their biggest stumbling block or challenge for launching their services is site rollout (yes touchy-feel infrastructure & real estate is a b*tch!). See also “Rakuten taking limited orders for services on its delayed Japan mobile network” (October, 2019).

Justin Garrison & Chris Nova, “Cloud Native Infrastructure”, 2018, O’Reilly and Kief Morris, “Infrastructure as Code”, 2016, O’Reilly. I am usually using both these books as my reference books when it comes to cloud native topics and refreshing my knowledge (and hopefully a bit of understanding).

Marshall W. Van Alstyne, Geoffrey G. Parker and Sangeet Paul Choudary, “Pipelines, Platforms and the New Rules of Strategy”, 2016, Harvard Business Review (April Issue).

Murat Uenlue, “The Complete Guide to the Revolutionary Platform Business Model”, 2017. Good read. Provides a great overview of platform business models and attempts systematically categorize platform businesses (e.g., Communications Platform, Social Platform, Search Platform, Open OS Platforms, Service Platforms, Asset Sharing Platforms, Payment Platforms, etc….).